With weak export growth, the gradual domestic demand recovery is supporting a widening trade deficit. The trade deficit in December came in at USD 0.8 billion, widening by USD 0.3 billion with respect to December 2023. The trade deficit came in between the Bloomberg median estimate of USD 0.9 billion and our forecast of USD 0.7 billion. As a result, the trade deficit came in at USD 10.8 billion, widening from the USD 9.7 billion recorded in 2023. At the margin, our seasonal adjustment shows the trade deficit at USD 12.2 billion (annualized; USD 9.8 billion recorded in 3Q24). Total imports (FOB) rose by 6.3% (+12% in November), boosted by imports of consumption goods, while transport equipment and construction imports fell. Export levels were broadly unchanged over one year in December, with coal exports still a drag.

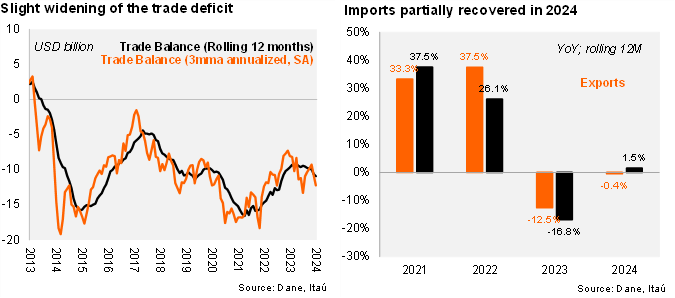

Total imports (FOB) increased 1.5% year-over-year in 2024, after the 16.8% fall in 2023. During the final quarter of 2024, imports grew 7.7% year-over-year (+5.6% in 3Q24 and 4.4% in 2Q24). At the margin, we estimate imports increased 25.4% qoq/saar, gaining momentum from the 15.9% decline in 3Q24 (+48.6% in 2Q24). The US accounted for 28.1% of total imports in 2024.

In 2024, exports contracted 0.4%, dragged by coal sales (-22% yoy). During the final quarter of 2024, exports increased 0.9% yoy (+2.8% yoy in 3Q24; +3.8% yoy in 2Q24). At the margin, exports grew by 8.7% qoq/saar during the final quarter (7.2% in 3Q24). The US accounted for 28.9% of total exports in 2024, rising 8% YoY.

Our take: The domestic demand recovery and weak commodity exports have led to a wider trade deficit. Nevertheless, we expect the CAD deficit to remain low at 2.0% of GDP in 2024, amid elevated remittances.