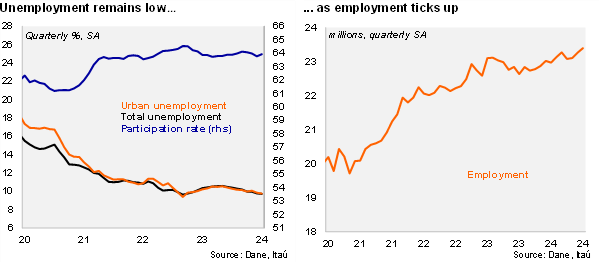

The national unemployment rate in December came in at 9.1%, down 0.9pp over one year, while the urban unemployment rate closed at 9.0% (dropping 1.2pp over one year). The urban unemployment rate was slightly below the Bloomberg market consensus and our call of 9.1%. National employment increased 3.3% yoy in December (+1.8% in November), while the labor force rose by 2.3% yoy (+0.9% previously). The participation rate increased by 0.5pp from December 2023 to 64.4%. Sequentially, employment increased 0.6% mom/sa from November, and rose 0.4% between 3Q24 and 4Q24. Meanwhile, the unemployment rate (SA) increased by 0.2pp from November to 9.7%. In 4Q24 the unemployment rate (SA) fell to 9.7%, down 0.3pp from 3Q24 (-0.6pp over one year), and remains below the NAIRU rate of 11.2% (SA), indicating that labor market continues to generate inflationary pressures.The unemployment rate for 2024 came in at 10.2%, stable from 2023.

Improving employment dynamics in 4Q24 lifted by services. During 4Q24, employment growth increased to 2.2% yoy, above from the 0.6% in 3Q24. The annual increase was pulled up by private salaried posts (+2.7% yoy; +2.1% in 3Q24), public sector jobs that rose by 1.9%, rebounding from the 5.2% annual contraction in 3Q24, and the self-employment increase of 1.9% (-0.3% in 3Q24). Real estate, information, communications, hotels, restaurants, and commerce activities were key job drivers in the 4Q24, while financial and insurance activities shed jobs.

Our Take: We expect the average unemployment rate to be steady at 10.2% this year. Contractionary monetary policy, along with a higher-than-expected minimum wage increase would likely limit labor demand.