Julio Ruiz

23/12/2022

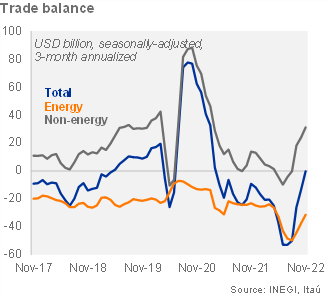

The monthly trade balance posted a deficit of USD 0.1 billion in November, narrower than market consensus of a deficit of 1.5 billion (as per Bloomberg) and our forecast of a deficit of USD 2.0 billion. The 12-month rolling trade balance stood at a deficit of USD 26.8 billion in November (practically unchanged from October), with the non-energy and energy balance at a surplus of USD 8.3 billion (from a surplus of 8.1 billion) and a deficit of USD 35.1 billion (from a deficit of USD 34.9 billion), respectively. At the margin, using three-month annualized seasonally adjusted figures, the trade balance improved to a deficit of USD 0.3 billion in November (from a deficit of USD 26.1 billion in 3Q22), with the energy trade deficit at USD 31.4 billion (from a deficit of USD 44.2 billion), while the non-energy trade balance posted a surplus of USD 31.1 billion (from a surplus of USD 18.1 billion).

Manufacturing exports deteriorated further in October. Using seasonally adjusted series, manufacturing exports fell by 0.9% mom (after contracting 4.5% in October), dragged by both vehicle (-1.5%) and non-vehicle (-0.6%) exports. The quarter-over-quarter annualized growth rate (qoq/saar) for manufacturing exports stood at 14.0% in October (from 16.9% in 3Q22).

Non-oil imports momentum is weak. Also using seasonally adjusted figures, non-energy imports fell by 3.5% mom/sa, taking the qoq/saar growth rate to -11.7% in November (from -5.1% in 3Q22). Looking at the breakdown, the qoq/saar of non-energy consumption, intermediate and capital imports stood at -16.0% in November (from 2.0% in 3Q22), -12.7% (from -6.7%) and 3.1% (from 1.8%), respectively.

We expect the trade deficit to deteriorate to USD 29 billion next year (from an estimated deficit of USD 25 billion in 2022). The weaker global outlook will curb manufacturing exports expansion, pressuring the trade deficit to the downside, which will be mitigated by a slower growth of non-energy imports as internal demand softens.

Julio Ruiz