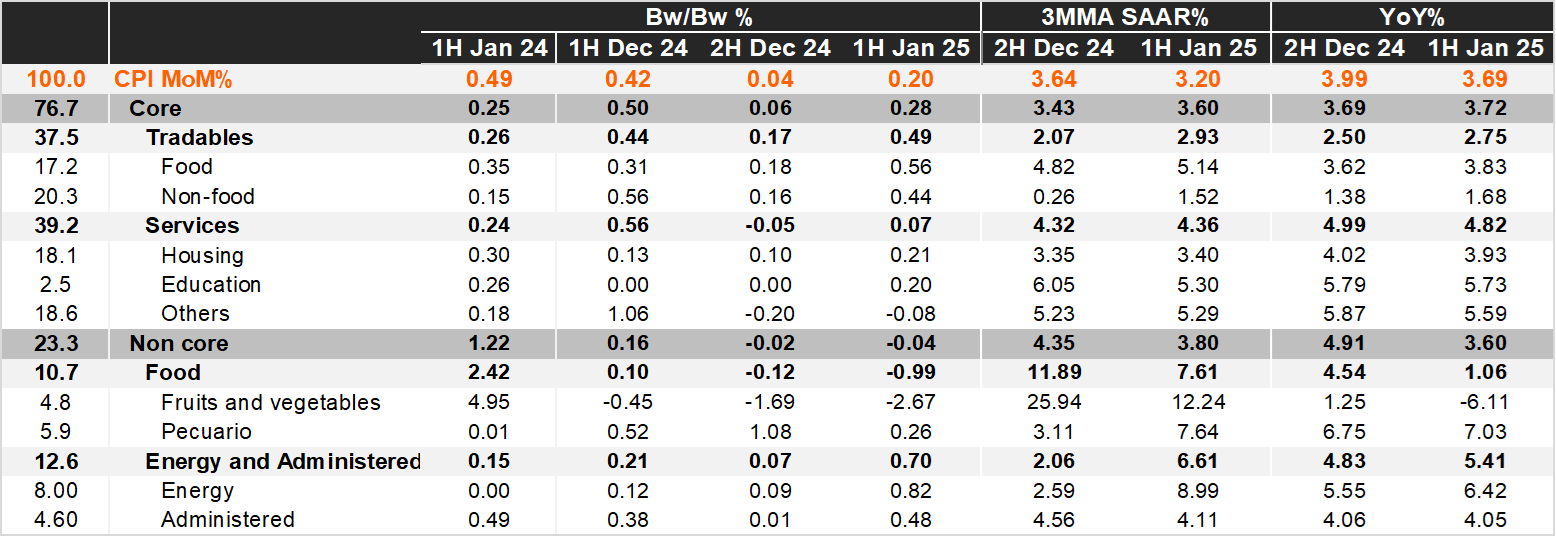

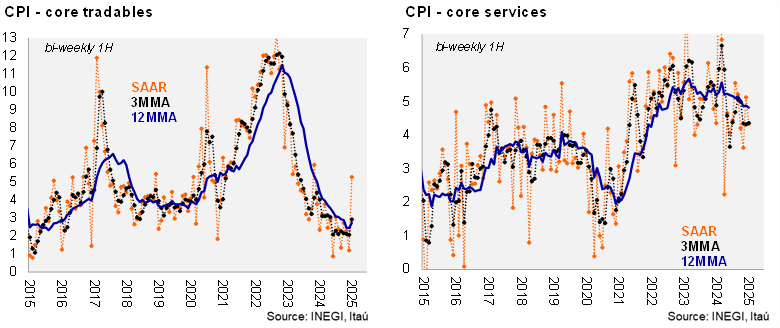

Bi-weekly headline CPI for the first half of January stood at 0.20%, below Bloomberg’s market consensus (0.27%) and our forecast (0.45%). The surprise relative to our number was concentrated in a higher-than-expected deflation on fruits and vegetables. Core inflation, on the other hand, came at 0.28%, between consensus (0.24%) and our forecast (0.34%). Inside the core component, tradables jumped 0.49% 2w/2w, already showing some early signs of pass-through following the weaker Peso. On the other hand, services were up 0.07% 2w/2w, with disinflation in other services despite an adverse beginning of the year seasonality. The non-core decreased 0.04% 2w/2w with relief on agricultural prices due to seasonal harvesting in products such as tomato and sugar, despite some pressures in livestock and energy and government tariffs.

Annual headline inflation reached 3.69% from 3.99% in the second half of December las year, consolidating below the ceiling of Banxico’s target. Core CPI was a bit up, from 3.69% in the previous fortnight to 3.72%, with merchandise at 2.75% (from 2.50%) and services at 4.82% (from 4.99%).

Our take: Today’s results support our view that the disinflationary trend continues, but the fundamentals, such as a weaker currency and a historically low unemployment rate, should limit a more significant deceleration. The current inflation dynamics, a more restrictive Fed, and the uncertainty about US trade policies (with a possibility of 25% tariffs on Feb 1st) will be key factors in the board’s upcoming decision. We expect a 25bps rate cut on February 6th to 9.75%. Moreover, we see five more cuts of 25bps during the year, with the reference rate to reach 8.5% at the end of the cycle.