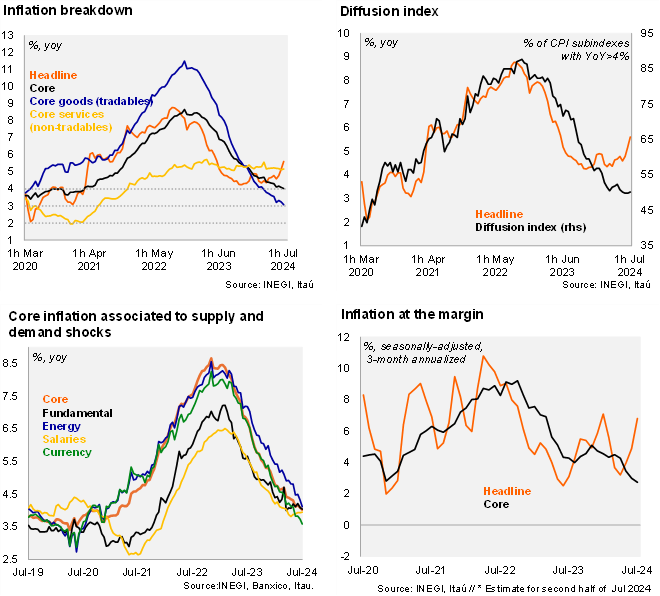

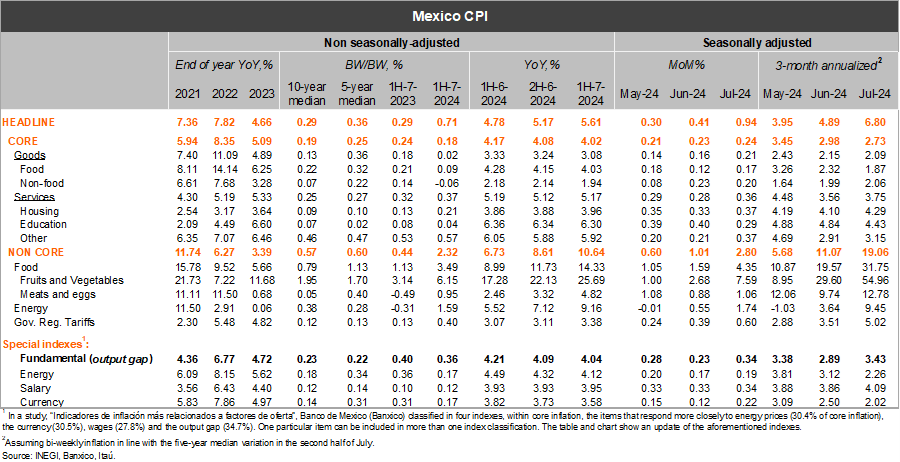

Bi-weekly headline inflation stood at 0.71%, above market consensus of 0.50% (as per Bloomberg), but closer to our call of 0.67%. Headline inflation was pressured mainly by the non-core index (2.32% bw/bw) which was driven by volatile fruits & vegetables (6.15% versus our call of 5.88%) and gas lp prices. On the other hand, core biweekly inflation stood at 0.18%, in line with market expectations (but slightly above our forecast of 0.23%). On an annual basis, headline inflation rebounded to 5.61% in 1H July (from 5.17% in 2H June) pressured by the non-core index, but with core inflation easing to 4.02% (from 4.08%). Within core inflation, the goods index was the main easing force (3.08%, from 3.24%), while services inflation remained persistent at 5.17% (from 5.12%). The latter is reflecting temporary pressure from airfares likely due to summer holidays. At the margin, assuming bi-weekly inflation in line with the five-year median variation in the second half of July, the seasonally adjusted three-month annualized headline inflation measure stood at 6.80% in July (from 4.89% in June), while core inflation fell to 2.73% (from 2.98%).

Our take: All in all, today’s figure should give some support for most Banxico members to cut its policy rate in the August 8 meeting. While headline inflation rebounded strongly, it was mainly due to the non-core fruits & vegetables volatile component, which should revert to the mean relatively quickly. Moreover, core inflation eased further, although with a persistent services inflation. The lower core inflationary gap amid a weaker activity outlook versus a highly restrictive stance should give space for a rate cut in August (our base scenario is for a 25-bp rate cut).

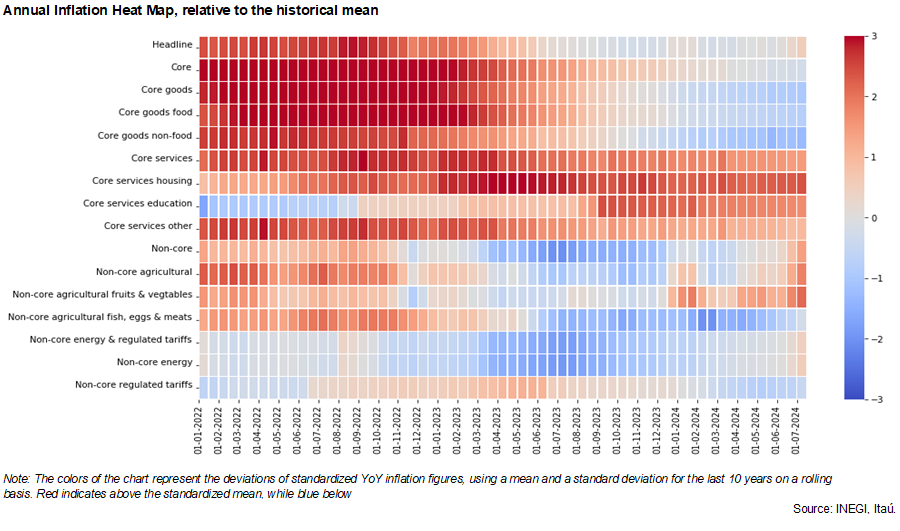

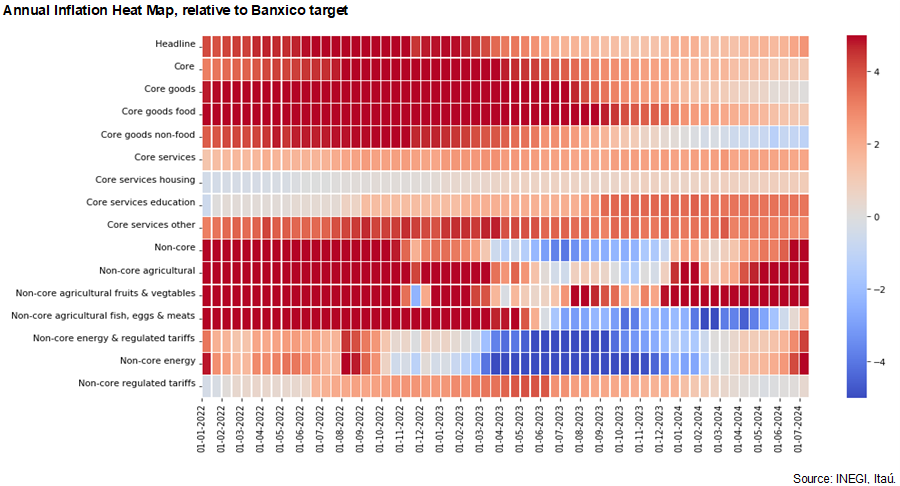

See detailed data below