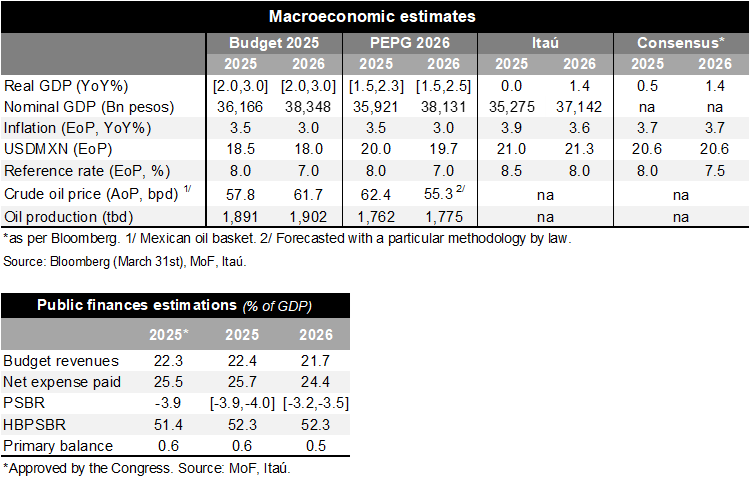

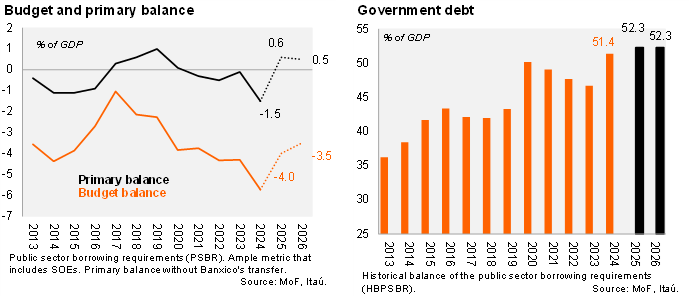

The Ministry of Finance (MoF) published the preliminary economic policy guidelines (PEPG), a document that updates the 2025 fiscal forecasts and guides the 2026 Budget due in September. The updated 2025 fiscal deficit forecasts were revised slightly below the approved budget. The nominal and primary fiscal deficits for 2025 are now projected to reach between -3.9% and -4.0% of GDP (previously at -3.9% of GDP) and 0.6% of GDP (unchanged), respectively. The narrowing of the fiscal deficits is explained by higher expenditures on social programs and public investment (25.7% of GDP, up from 25.5% of GDP), which offseted slightly higher revenues (22.4% of GDP, up from 22.3% of GDP). The latter is supported by higher oil prices, despite an expectation of lower domestic production, and an assumption of a more depreciated currency, all relative to the approved budget. The modest improvement in tax revenues is explained by contradictory factors, including a differentiated tax rate from countries without a trade agreement with Mexico and lower excise gasoline tax revenues expected to smooth retail gasoline prices amid higher energy prices.

The MoF warned that U.S. trade policies could impact revenues going forward, but they did not include this in their forecast. In today’s conference call with investors, the Chief Economist at the MoF mentioned that this risk is likely to be included in the September budget, following today’s announcement by Trump and potential retaliatory measures from the Mexican government.

Additionally, we note that within fiscal expenditures, the financial cost estimate was increased from 3.8% to 3.9% of GDP due to the depreciation of the exchange rate, which implies a higher increase in programable expenditure. The broadest measure of debt, the Historical Balance of Public Sector Borrowing Requirements (HBPSBR), for the end of this year was revised up to 52.3% of GDP (previously at 51.4%).

The fiscal consolidation for 2026 was revised to a range of -3.9% to -3.5% (from -3.9%) relative to the forecasts announced in the approved 2025 budget, with a primary surplus of 0.5% (unchanged), while the HBPSBR was projected at 52.3%, up from 51.4%. We note that the document includes a preliminary list of priority expenditure programs in preparation for the 2026 budget due next September. This list includes several social priority programs, such as migratory services and the defense of Mexico’s interests in the multilateral arena, along with the continuation of AMLO’s social programs.

Our view: Despite the fiscal consolidation signal remaining with a lower budget balance from 2024 (-5.7% to -4.0% of GDP), there is an acknowledgment of a more challenging outlook where expenses might increase more than anticipated in the 2025 budget, while revenues see only a modest increase this year (in an optimistic close to 2.0% GDP growth scenario). Consequently, government debt is expected to rise to 52.3% of GDP (from 51.4%) in 2025, the highest level in over 20 years, which will likely lead to a one-notch downgrade by the rating agencies this year. During AMLO’s administration, a 50% of GDP threshold was imposed by the government, which made rating agencies more comfortable, so changes in the debt pose a relevant risk. Our nominal fiscal deficit forecast of 3.9% of GDP for this year has a slight upward bias (higher deficit) considering the challenges from the U.S. trade policy and the 2026 PEPG. On the other hand, the main risk for 2026 comes from the revenue side, with less room for efficiency measures and increasing spending from social programs, particularly those for elderly people. The 2026 fiscal projections are to be delivered along with the 2026 budget, due in September.

See details below

Julia Passabom

Mariana Ramirez