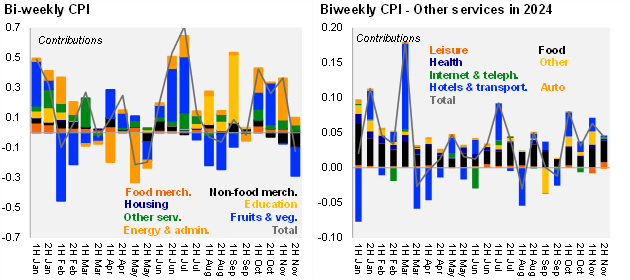

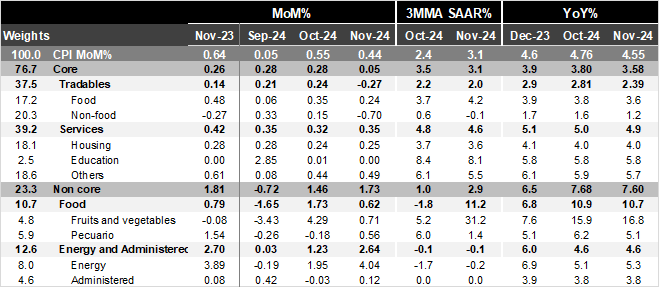

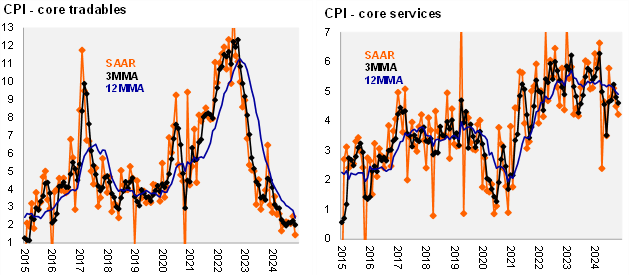

Headline CPI stood at 0.44% MoM in November, slightly below Bloomberg’s market consensus of 0.47% and close to our forecast of 0.43%. The monthly number is consistent with a bi-weekly 0.12% deflation. Core inflation was up 0.05% MoM, also marginally below market expectations of 0.07% due to non-food merchandise in heterogeneous items, such as televisions and clothes (most due to “El Buen Fin” temporary impact). Non-core inflation was up 1.73% MoM due to livestock prices; on the other hand, agricultural prices fell due to the rainy season and a higher crop availability. On an annual basis, headline inflation declined to 4.55%, from 4.76% in the previous month, while core inflation fell to 3.58%, a level not seen since 2020. Other services surprised to the downside in items such as internet and auto services. Banxico’s forecast of 4.7% YoY for headline inflation and 3.7% YoY for core inflation in the 4Q is in line with Oct-Nov figures of 4.66% YoY and 3.69% YoY, respectively.

Our take: Mexico’s CPI continues to show a lower goods inflation, in line with a still numb pass-through, while services inflation shows some incipient signs of deceleration. All in all, the print favours an acceleration to a 50bps cut from Banxico at the last meeting in the year.