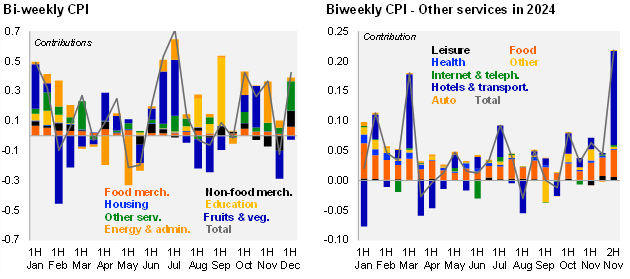

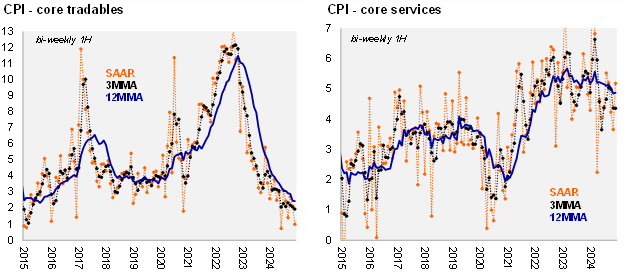

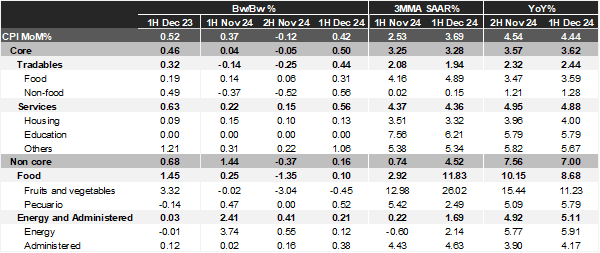

Bi-weekly headline CPI came at 0.42% in the first half of December, between Bloomberg’s market consensus (0.36%) and our forecast (0.46%). Core inflation rose 0.50% (market: 0.47%, Itaú: 0.55%), due to a payback from “El Buen Fin” discounts that affected the non-food merchandise component and Christmas Holidays with effects in tourism (hotels and transportations). Non-core inflation rose by 0.16% due to livestock prices, while agricultural prices fell due to higher crop availability. On an annual basis, headline inflation continues to trend down, falling to 4.44% from 4.54% in the 2H of November. In contrast, core inflation rose to 3.62%, from 3.57%. Data implies a quarterly average for headline at 4.61% YoY and 3.68% YoY for the core, both consistent with Banxico’s forecast from last week’s decision (4.6% and 3.6%, respectively).

Our take: Today’s results were mostly positive, as seasonal increases were balanced by other favorable factors such as crop availability in products like avocado, beans and corn used for livestock feed. We keep our year-end forecast at 4.3% YoY. Given today's release and Banxico’s statement last week, opening the door for larger cuts ahead, we expect a 50bps cut in February. The risk remains at tighter global financial conditions preventing an acceleration next year.