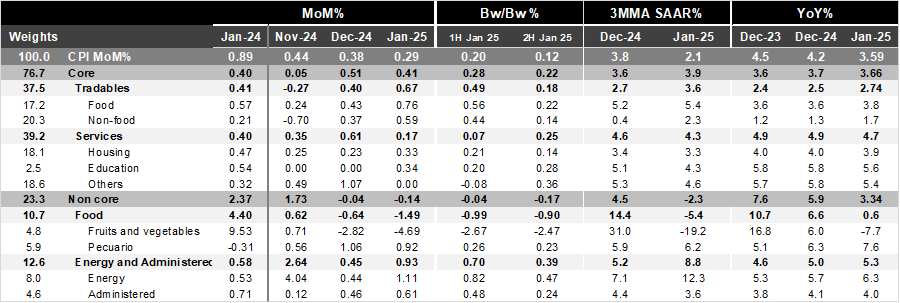

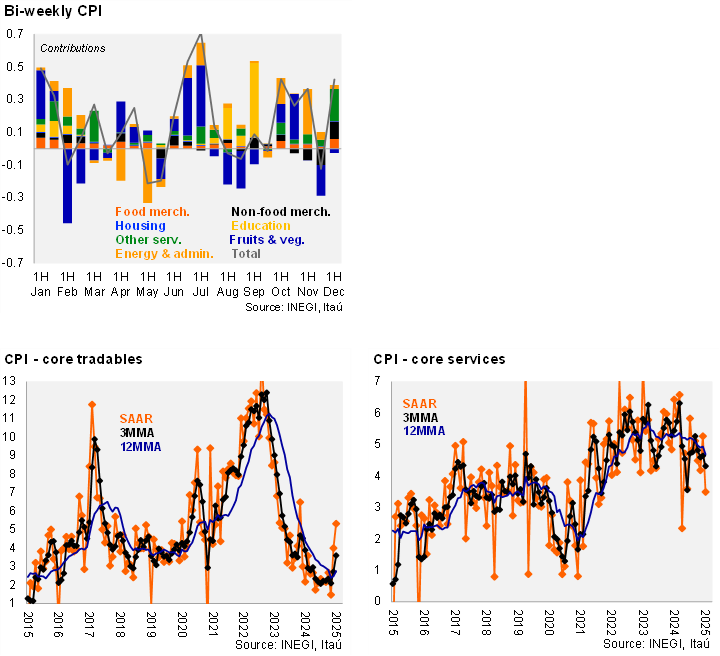

Bi-weekly headline CPI for the second half of January stood at 0.12%, below Bloomberg’s market consensus (0.19%) and our forecast (0.22%). Core inflation came at 0.22%, a bit lower than consensus (0.26%) and closer to our forecast (0.23%). Inside the core component, tradables prices decelerated to 0.18% 2w/2w from 0.49% in the last fortnight. On the other hand, services prices were up by 0.25% 2w/2w, with pressures in other services after two fortnights of deflation. The non-core fell by 0.17% 2w/2w with relief on agricultural prices due to seasonal harvesting, despite the pressure in livestock and energy, while government tariffs continue to pressure the group.

In January, annual headline inflation reached 3.59%, down from 4.21% in December 2024, consolidating below the ceiling of Banxico’s target. Core CPI was a bit up, from 3.65% in December to 3.66% in January, with merchandise at 2.74% (from 2.47%) and services at 4.69% (from 4.94%). In yesterday’s statement, Banxico forecast 3.7% for headline and 3.6% for core during the 1Q25, achievable considering today’s release.

Our take: Today’s results showed that the disinflationary trend is in motion, also supported by a deceleration in economic activity, especially in the last quarter of 2024. The inflation scenario, however, remains challenging, with the Peso depreciation and tight labor market posing risks. We forecast CPI will end 2025 at 3.9%. For the interest rate, since the board incorporated a larger weight of the economic deceleration in its reaction function and reinforced the downward trend in inflation, we reiterate our call for a 50bps cut rate on March 27th, taking the interest rate to 9.0% and 25 bps after that, with the year-end forecast at 8.50%.