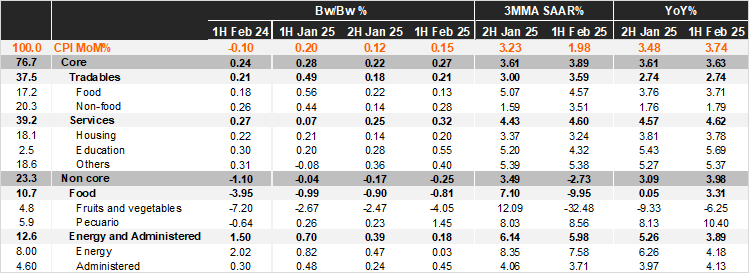

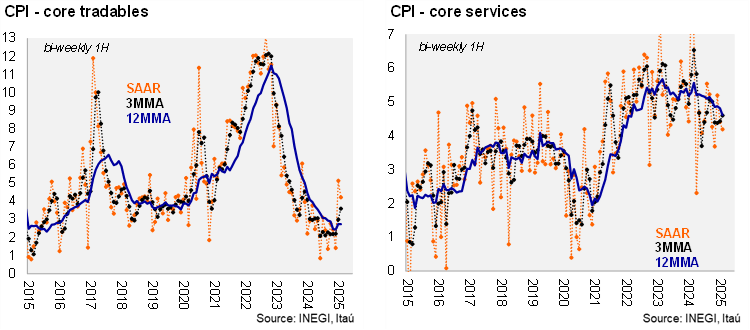

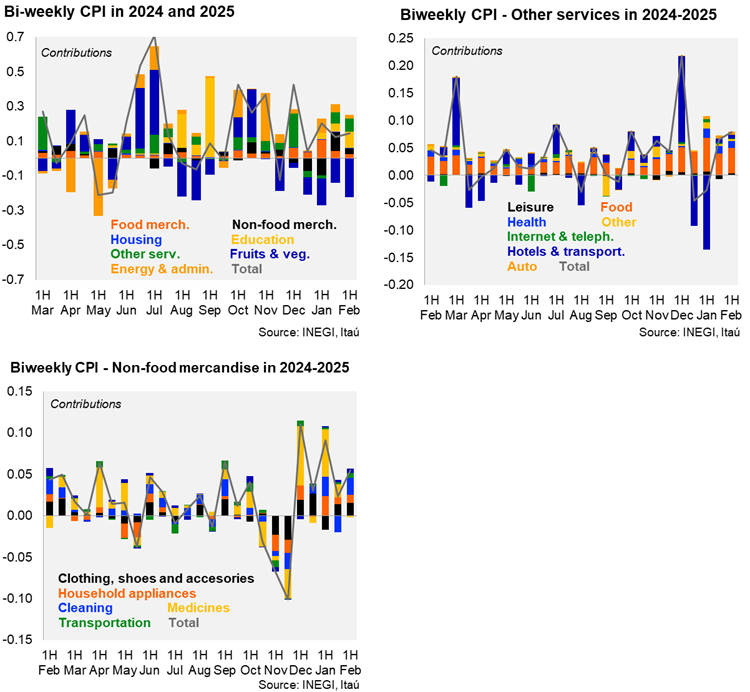

Bi-weekly headline CPI for the first half of February stood at 0.15%, a tad below Bloomberg’s market consensus (0.17%) and our forecast (0.18%). On the other hand, core inflation came at 0.27%, a bit higher than consensus (0.25%) and our forecast (0.17%). Inside the core component, tradables prices accelerated 0.21% 2w/2w, from 0.18% in the last fortnight, with a seasonality rebound after the end of winter season discounts. Services prices were up by 0.32% 2w/2w, from 0.35%, with pressures in other services for two fortnights in a row. The non-core fell by 0.25% 2w/2w with relief on agricultural prices due to downward seasonality in tomatoes and onions, despite the pressure on livestock, in items such as egg and meat, while energy and government tariffs continue to pressure the group.

In annual terms, headline inflation accelerated to 3.74%, from 3.48% in the second half of January, but still below the ceiling of Banxico’s target. Core CPI was also a bit up, from 3.61% in the previous fortnight to 3.63% now, with merchandise at 2.74% (no changes) and services at 4.62% (from 4.57%). In the February 6th statement, Banxico forecasted 3.7% for headline and 3.6% for core during the 1Q25, achievable considering today’s release.

Our take: Today’s print indicates that the disinflationary trend is gaining momentum, supported by low agricultural prices and partially supported by a slowdown in economic activity. However, the inflation outlook remains challenging, with the peso depreciation, volatile climate conditions with draughts in some parts of the country, and tight labor market posing risks ahead. We forecast CPI to end 2025 at 3.9%. For the interest rate, we maintain our call for a 50bps cut rate on March 27th, taking the interest rate to 9.0% and 25 bps after that, with the year-end forecast at 8.50%.