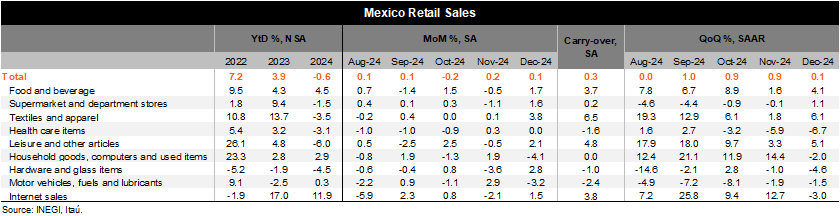

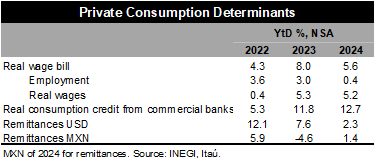

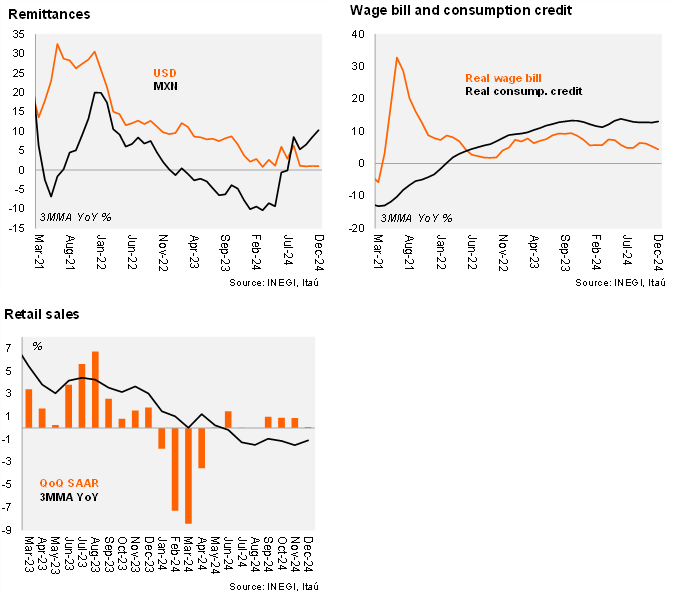

Retail sales fell 0.2% YoY in December, a smaller contraction than Bloomberg’s median of surveyed analysts (-1.5%). On a monthly basis and using seasonally adjusted figures, retail sales increased 0.1%, better than the consensus forecast (-0.4%). Six out of nine subsectors were up, highlighting textile and apparel at 3.8%, hardware and glass items at 2.8%, and leisure and other articles at 2.1%. On the other hand, household goods and motor vehicles were down at 4.1 and 3.2% MoM, respectively. Looking ahead, most private consumption determinants remain supportive, with the 2024 YtD of the real wage bill at 5.6%, while real consumption credit from commercial banks and remittances in MXN stood at 12.7% and 1.4%, respectively. The better-than-expected performance can be attributed to the exchange rate depreciation and the newly implemented tax rate for marketplaces from countries without a trade agreement with Mexico. Both factors contributed to higher consumption of domestic goods in department stores.

Our take: Consumption ended 2024 slightly positive with the QoQ/SAAR at 0.1% (from 0.9% in the previous quarter), with a statistical carry-over of 0.3%. Due to resilient consumption determinants, namely the growing real wage bill, historically high consumer confidence, and tariffs on goods from non-treaty countries implemented in December, we expect the sector to remain slightly on positive terms in 2025. Furthermore, we expect private consumption to be the main driver for GDP this year. Our GDP growth forecast for 2025 stands at 0.9% YoY.

See detailed data below