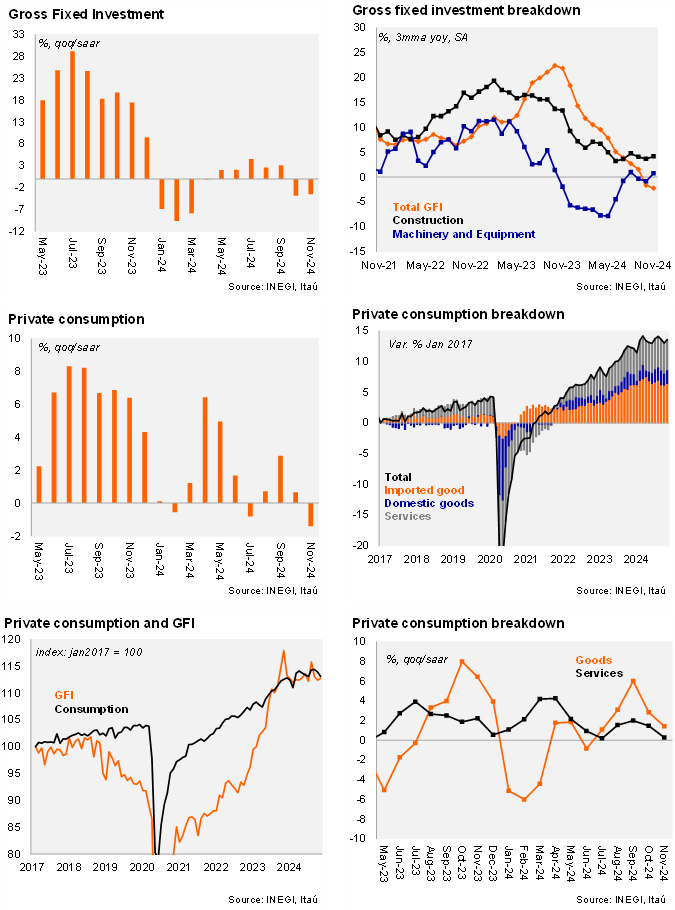

Gross Fixed Investment (GFI) contracted by 0.7% YoY in November, falling less than the Bloomberg consensus and our forecast (both at -1.2%). By sectors, machinery and equipment increased 5.8%, with both imported and national aggregations up. However, construction decreased by 6.0% YoY with public and non-residential components down. Using seasonally adjusted data, investment rose by a modest 0.1% MoM, better than market expectations (-0.2%), following a +0.3% increase in October. Machinery and equipment increased 1.7% MoM, while construction declined 1.0%, with both residential (-2.0%) and non-residential as a drag (-0.3%), mainly explained by the end of public infrastructure projects.

On the other hand, private consumption rose by +0.3% YoY in November, increasing less than the Bloomberg consensus (+1.0%) and our forecast (+0.8%). On a monthly basis, private consumption rose 0.5%, after two months of contractions, with increases in services (0.1%), domestic goods (0.5%), and imported goods (1.7%), despite the peso depreciation and demand preferences shifting to international goods at the margin.

Our view: Today’s figures showed that domestic demand continued to slow at the end of last year, with both investment and consumption down QoQ/SAAR at -3.5% and -1.4%, respectively. Headwinds that affected activity in 4Q24 are likely to persist in 2025, with consumption as the main driver of domestic demand due to still positive fundamentals, while investment should slow due to fewer infrastructure projects and heightened domestic and external policy uncertainty.