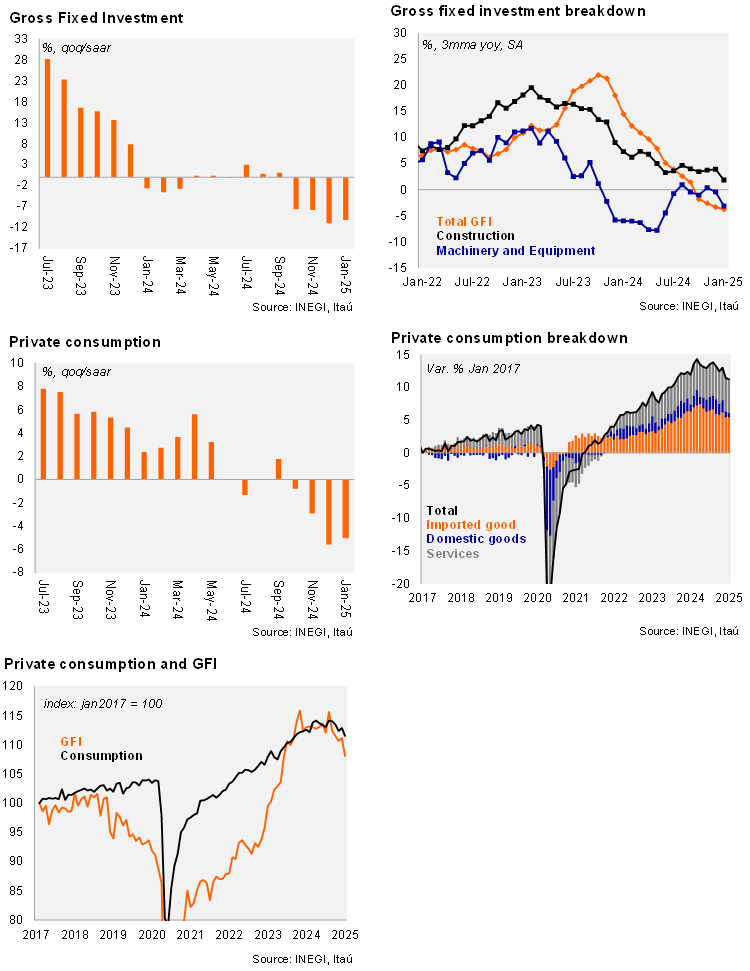

Gross Fixed Investment (GFI) fell by 6.7% YoY in January, a deeper contraction compared to Bloomberg’s consensus of -5.7%. By sector, machinery and equipment decreased by 3.2%, with both imported and domestic components down. Construction fell further (-9.9% YoY), with public and non-residential components declining. Using seasonally adjusted data, investment decreased by 1.5% MoM, in line with market expectations. Machinery and equipment fell by 1.8% MoM, while construction declined by 1.4%, with non-residential construction acting as a drag (-3.2%) due to the completion of public infrastructure projects from AMLO’s administration.

Private consumption stood at -1.3% YoY, a deeper contraction than the consensus of -0.4%. On a monthly basis, private consumption decreased by 0.3%, marking a decline for two consecutive months, with decreases in both domestic goods (-0.4%) and imported goods (-0.1%). However, services increased by 0.2%, maintaining a positive trend.

Our view: January domestic demand figures showed weak results for the start of 1Q25, with investment down 10.2% QoQ/SAAR and consumption down 5.0%. These results followed other weak data at the beginning of 2025, such as industrial production and monthly GDP. We forecast a 0.5% QoQ SA GDP contraction in the first quarter, indicating a technical recession following the 0.6% decline in 4Q24. Looking ahead, economic activity could improve if uncertainties regarding trade policy moderates materially, which might support private investment and internationally related sectors. For 2025 we forecast 0.0% GDP growth but acknowledge sizeable downside risks.

See details below