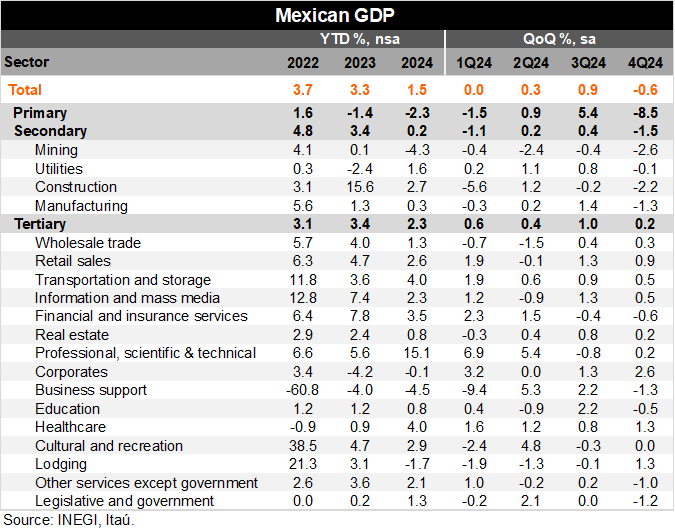

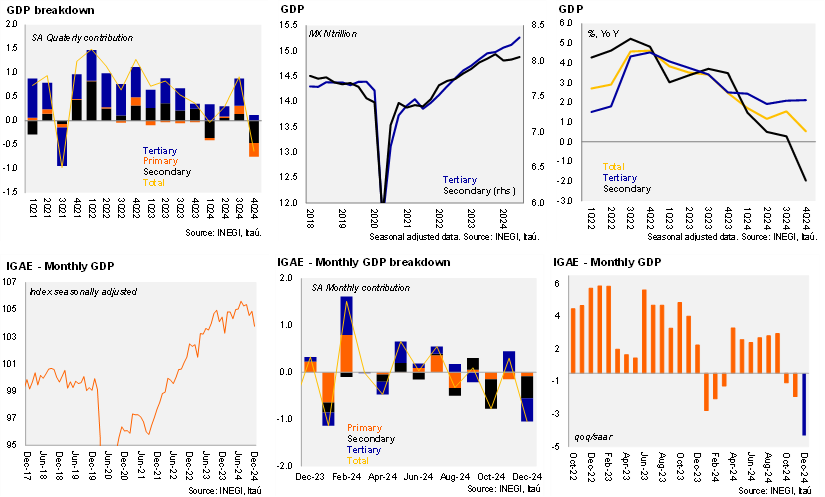

The 4Q24 final GDP rose 0.5% YoY, a tad lower than Bloomberg’s market consensus and the preliminary release (both at 0.6%) but in line with our forecast. This represents a deceleration relative to 3Q24 (1.5% YoY) due to supply shocks that affected the quarter, naming hurricanes, closure of roads, and strikes. Primary activities stood at -4.1% YoY (preliminary: -4.6%), industry at -2.0% YoY (preliminary: -1.7%) and services at +2.1% YoY (no changes from preliminary data). Using seasonally adjusted data, GDP decreased 0.6% QoQ (in line with the preliminary estimation), with industry and primary activities as the main drags at -8.5% and -1.5%, respectively (preliminary: -8.9 and -1.2%), while services contributed slightly positively with a quarterly growth of 0.2% (no changes). The full year rose 1.5% YoY, a deceleration from 2023 and 2022 (3.3 and 3.7%, respectively).

According to the monthly GDP (IGAE), the economy decreased 0.4% YoY in December, lower than both the consensus (+0.20%) and our forecast (+0.10%). On a monthly basis, IGAE contracted 1.0%, with a broad-based decrease within its subsectors: industry (-1.4%), primary activities (-2.0%) and services (-0.8%). The QoQ/SAAR stood at -3.8% in the 4Q24, from -1.4% in the previous quarter.

Our take: Looking ahead, we anticipate that the economy will grow at a moderate pace in 2025, mainly driven by consumption and services, supported by positive factors such as rising real wages and still solid consumer confidence. The statistical carry-over for 2025 after today’s release is at only 0.1%. We forecast GDP to grow 0.9% in 2025, though with a downside risks due to challenges related to US trade going forward. With this economic deceleration in mind and the recent Board communication, we forecast a 50bps cut at the next Banxico meeting (March 27th, to 9.0%).

See detailed data below