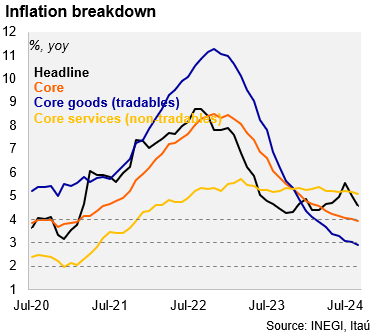

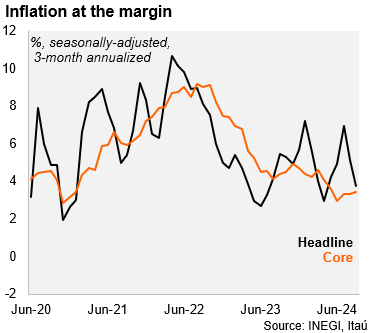

Monthly headline CPI rose by 0.05% MoM, below market expectations of 0.08% according to the Bloomberg median. Core inflation rose by 0.28%, also below the Bloomberg median of 0.31%. On an annual basis, headline inflation fell further to 4.58% (from 4.99% in August), the lowest print since March (4.42%). Core inflation fell to 3.91% (from 3.99% in August), mainly driven by the decline in core goods inflation (2.92% in September), as core services remain sticky (5.1%). Our seasonally adjusted 3-month annualized headline inflation metric came in at 3.77% (down from 5.16% in July), while the same metric for core rose to 3.43% (from 3.32% in July).

Our take: Even though inflation in Mexico has broadly surprised to the downside since August, the data does not change our view for the gradual disinflationary process to continue in the short-term. Gradually lower inflation prints take place as survey-based inflation expectations at the one-year horizon have also edged lower, especially core, consistent with persistent downside revisions to activity. We expect Banxico to continue cutting the monetary policy rate at a 25-bps pace in the next monetary policy meeting (November 14). We expect CPI to end the year at 4.3%, essentially in line with Banxico’s 4.4% 4Q24 average.

Andrés Pérez M.