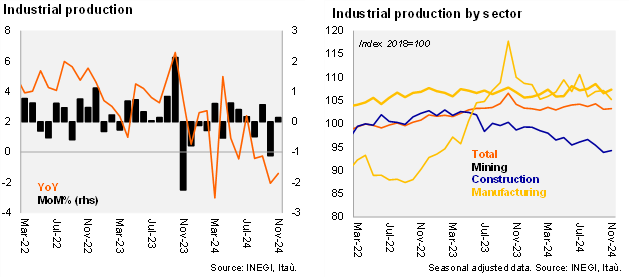

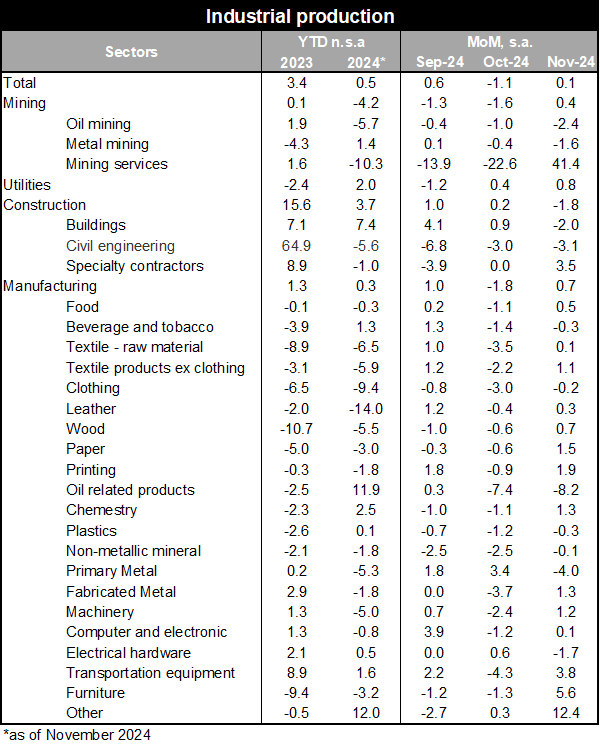

Industrial production (IP) decreased by 1.4% YoY in November, broadly in line with Bloomberg’s market consensus and our forecast. Inside the annual figure, mining led the performance at -4.7%, followed by construction (-4.2%) and manufacturing (-0.2%). At the margin, using seasonally adjusted figures, IP stood almost stable (+0.1% MoM), after falling 1.1% in October, supported by mining (+0.4%, although with high volatility in construction of oil related projects), and manufacturing (+0.7%, with fourteen out of twenty-one subsectors in positive terms). Construction plummeted 1.8% MoM, after positive numbers in the two previous months, due to additional weakness in civil engineering and buildings explained by the finalization of public projects and a high base effect. Momentum in IP remains weak as of November, with the QoQ/SAAR at -1.6% (from -1.0% in the previous quarter).

Our take: The IP data release today confirms the softening of economic activity by the end of 2024. We expect GDP to grow 1.4% YoY in 4Q24 (year-end 1.7%). Although activity is weak at the margin, some fundamentals for growth, such as wage bill dynamics, remittances, consumer confidence, credit, and exports, remain at solid levels, which should continue to provide some support for growth in 2025 (we forecast 1.5% GDP this year).

See detailed data below