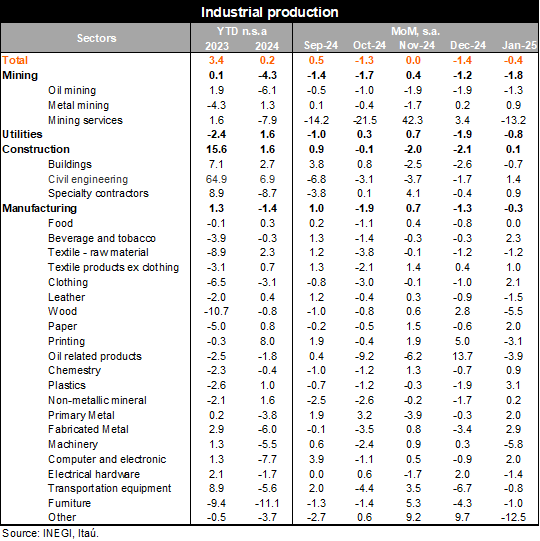

Industrial production (IP) fell by 2.9% YoY in January, a deeper contraction than Bloomberg’s market consensus (-1.7%) and our forecast (-1.5%). Inside the annual figure, three components explained the bad performance: construction (-6.7%), mining (-8.8%), and manufacturing (-0.8%), while utilities increased by 0.8% (from +1.7% in December).

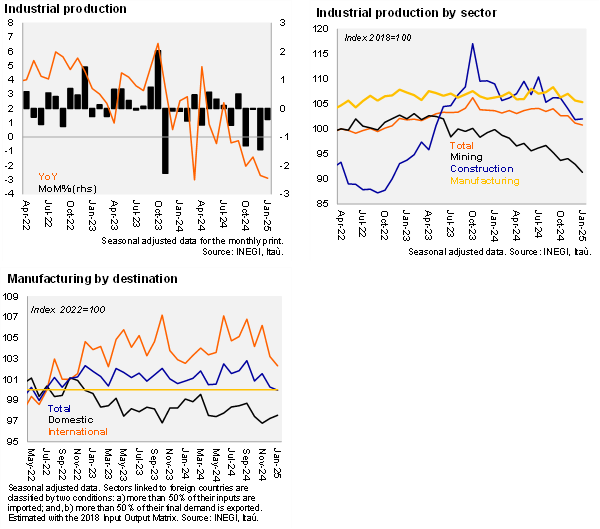

Using seasonally adjusted figures, IP decreased 0.4% MoM, after a large contraction in December of 1.4% and surprised negatively considering the INEGI’s nowcast of +0.1% MoM. This negative performance was explained by mining (-1.8%, with oil and services as the main drags), manufacturing (-0.3% MoM, with 9 out of 21 subsectors decreasing) and utilities (-0.8%), that couldn’t be offset by construction (+0.1%, benefited from civil engineering and specialty contractors). Momentum in the industry sector remained weak in January, with the QoQ/SAAR at -7.2% from -6.6% in December.

Our take: Today’s IP print reinforces our view that the Mexican economy is losing strength since the 4Q24. We expect that, in the beginning of 2025, the threat of tariffs from the US will also generate distortions in manufacturing exports such as temporary inventory accumulation and a reorganization of supply chains. Also, high uncertainty is likely to be reflected in low levels of private investment, which should imply weak building construction and manufacturing levels ahead.

See more details below