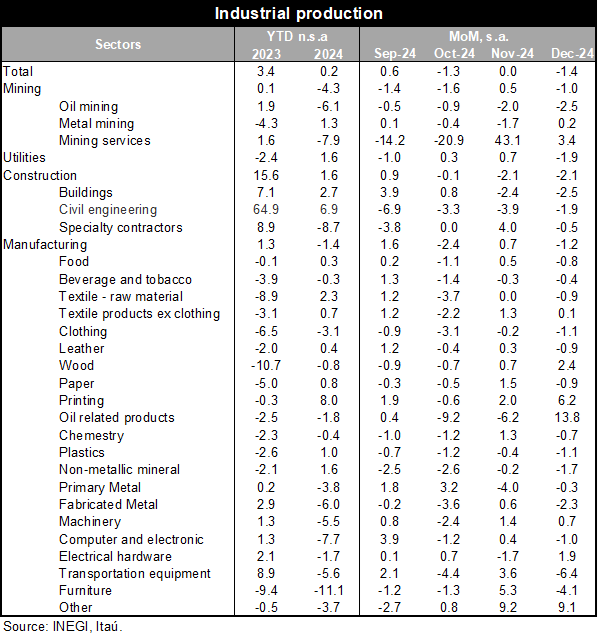

Industrial production (IP) fell by 2.7% YoY in December, a deeper contraction than Bloomberg’s market consensus and our forecast (both at -1.2%). Inside the annual figure, construction led the bad performance (-7.5%), followed by mining (-6.3%), and manufacturing (-0.6%), while utilities increased by 1.7%. With this print, IP grew only 0.2% in 2024, a significant moderation from the 3.4% in 2023, with mining and manufacturing as the main drags.

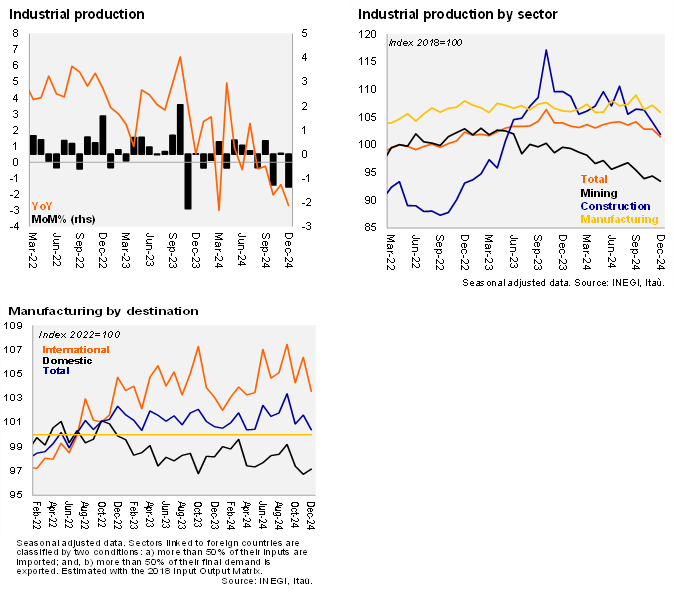

Using seasonally adjusted figures, IP decreased 1.4% MoM (consensus at -0.5%), after a null result in November and lower than INEGI’s nowcast of +0.3% MoM. This result was explained by contractions in every sector: construction (-2.1%, with all its subsectors decreasing), mining (-1.0%, with headwinds from oil mining), and manufacturing (-1.2% MoM, with fourteen out of twenty-one subsectors contracting). Momentum in the industry sector remained weak as of December, with the QoQ/SAAR at -6.1% (from -2.5% in the previous quarter).

Our take: Today’s IP print reinforces that the downward trend on activity data at the end of 2024 was deeper than expected. Looking ahead, the threat of tariffs from the US could also generate distortions in manufacturing exports such as temporary inventory accumulation and a pause in investment. However, peso depreciation and positive external demand should provide some support to IP in the coming months. We also expect that positive fundamentals, such as increasing wage bill and positive credit dynamics from the commercial bank, could benefit the services sector in 2025, partially offsetting the high external uncertainty.

See details below