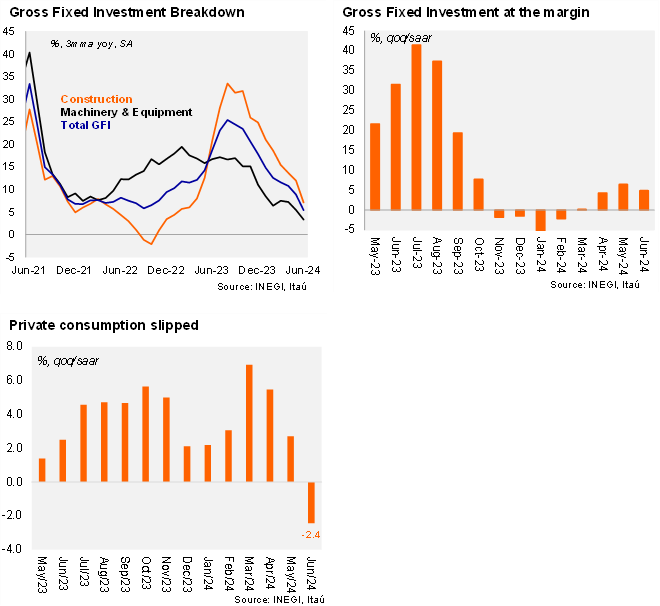

Gross Fixed Investment (GFI) fell by 1.3% yoy in June (vs. market consensus of -1.2%), while the private consumption proxy rose by 0.4% (vs. market consensus of 0.8%). According to the seasonally adjusted series, GFI contracted by 1.0% MoM/SA in June (+1.3% in May), driven by construction investment (-3.2% MoM/SA), while machinery & equipment rose by 1.6%. GFI momentum decelerated at the margin, with the qoq/saar at 4.9% in June (from 6.4% in the quarter ending in May). In contrast, private consumption rose at the margin by 0.1% MoM/SA in June, after two consecutive monthly declines in April and May. The sequential recovery was mainly driven by growth in goods (0.6% MoM/SA), with lower growth in services (0.1% MoM/SA), as the drag in imported goods and consumption of services contracted for the third consecutive month. Private consumption momentum slipped further, with the qoq/saar falling by 2.4% in June (from +2.7% in the quarter ending in May), the first sequential contraction since the post-pandemic recovery.

Our take: The weakening of internal demand, reflected by the sequential contraction of private consumption and a gradual deceleration of gross fixed investment, should lead Banxico to continue easing. Our base case remains for a 25-bp rate cut in the September 26 meeting. INEGI will publish July data on GFI and private consumption on October 2.