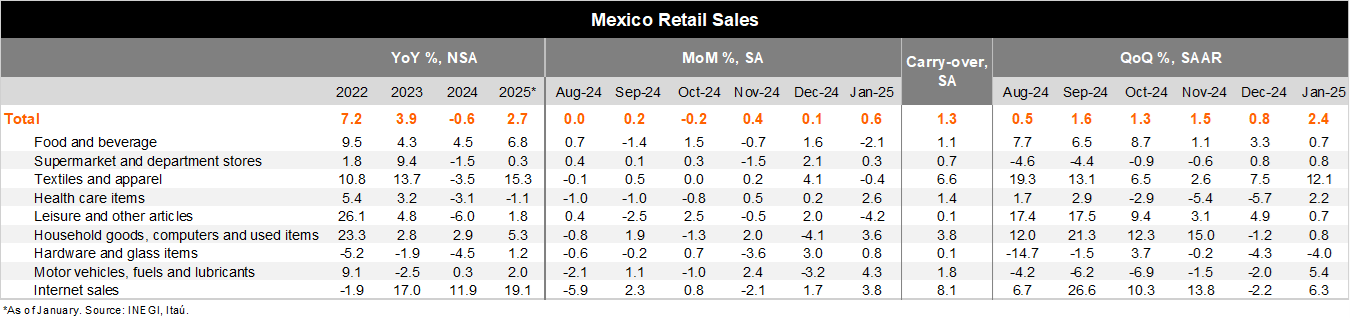

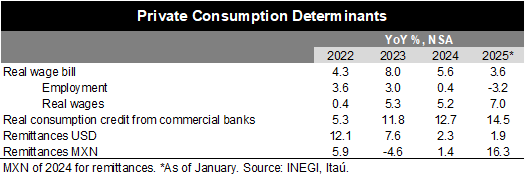

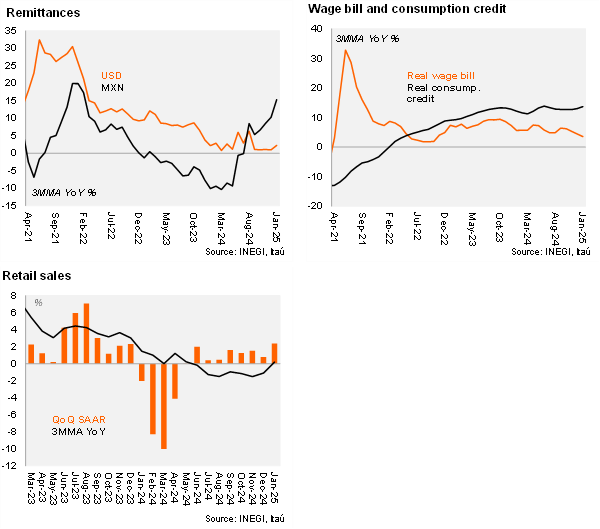

Retail sales rose 2.7% YoY in January, surprising analysts who had predicted a 1.1% increase according to Bloomberg’s median survey. Of note, retail sales data surprised to the upside for the second consecutive month. On a monthly basis, using seasonally adjusted figures, retail sales increased by 0.6%, above the consensus forecast of 0.0%. Six out of nine subsectors grew in January, with household goods up by 3.6%, motor vehicles by 4.3%, and internet sales by 3.8%. However, leisure, food, and beverage items experienced contractions of 4.2% and 2.1% MoM, respectively. The better-than-expected performance can be attributed to positive private consumption determinants that remain supportive, with the real wage bill rising by 3.6% YoY, and real consumption credit from commercial banks and remittances in MXN at 14.5% and 16.3%, respectively.

Our take: In contrast to recent supply-side data (see here) has been softer than expected, private consumption started positively in 2025, with the QoQ/SAAR at 2.4% (up from 0.8% in the previous quarter), and a statistical carry-over of 1.3% for the year. Due to resilient consumption determinants, such as the growing real wage bill, historically high consumer confidence, and tariffs on goods from non-treaty countries implemented in December to support domestic consumption, we anticipate the sector to remain slightly positive in 2025. Additionally, we expect private consumption to be the main driver for GDP growth this year. Our forecast indicates a GDP growth of 0.0% YoY in 2025.

See detailed data below