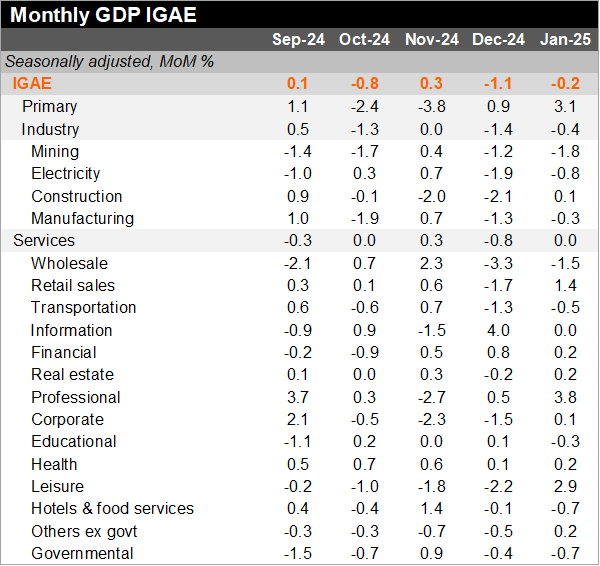

Economic activity fell by 0.1% YoY in January, in line with our estimate and a tad lower than Bloomberg’s market consensus of -0.02%. In terms of sectors, services increased by 0.8% YoY, with 10 out of 14 subsectors showing improvement supported by positive fundamentals. Industry decreased by 2.9% YoY to the lowest level since March 2024. The decline was driven by mining, construction, and manufacturing, partly due to negative base effects and trade uncertainties. The primary sector rebounded by 14.8% YoY, despite cold weather in some parts of the country.

When considering seasonally adjusted figures, the economy contracted by 0.2% MoM (IGAE nowcast at +0.1% MoM). In terms of sectors, the industrial production fell by 0.4% MoM due to declines in construction and mining. Services remained unchanged from the previous month, despite positive performances in retail sales, professional services, and leisure subsectors. Primary activities increased by 3.1% MoM, up from 0.9% in December.

In addition, INEGI published its February nowcast for manufacturing, which decreased by 2.4% YoY, taking the index down to the lowest level since December 2023, following a 0.8% decline in January.

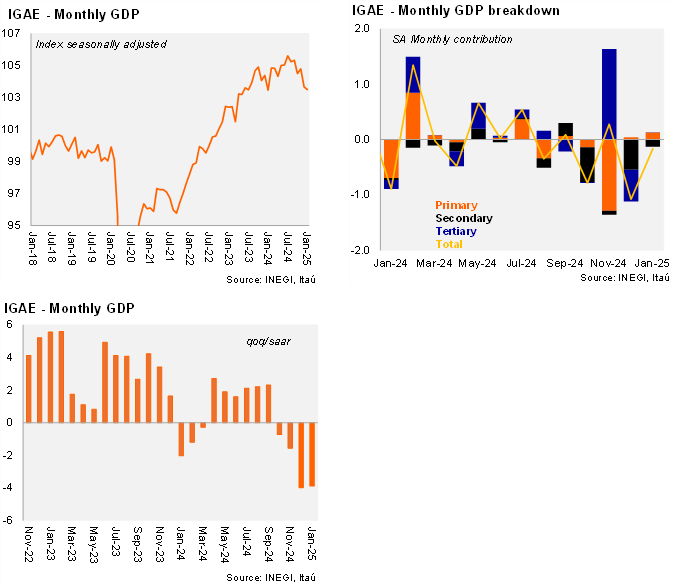

Our view: Today’s results confirm our view that the economy is continuing to decelerate at the start of 2025. Based on the data released today, we are forecasting a 0.5% QoQ SA contraction in the first quarter, indicating a technical recession following the 0.6% decline in 4Q24. Looking ahead, the economic activity could improve if uncertainties regarding trade policy disappear, which might support private investment and internationally related sectors. For 2025, we maintain our GDP forecast of 0.0%.

See details below