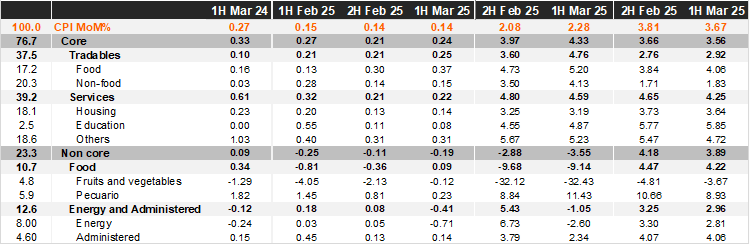

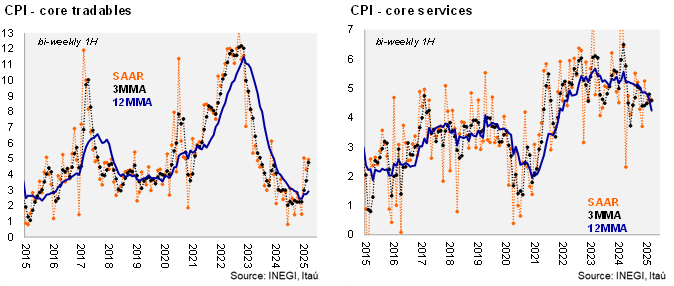

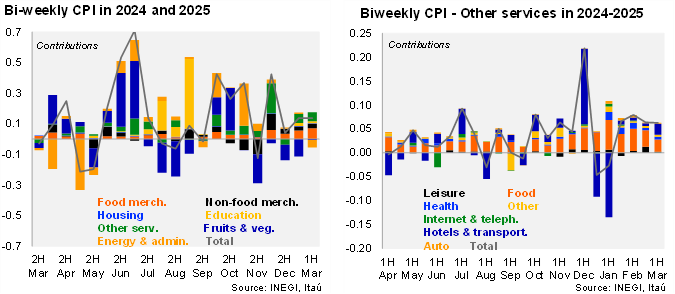

Bi-weekly headline CPI for the first half of March was 0.14%, between Bloomberg’s market consensus (0.17%) and our call (0.08%). Core inflation came in at 0.24%, close to expectations (market at 0.25% and our forecast at 0.22%). Within the core component, tradables prices were up 0.15% 2w/2w, from 0.14% in the previous fortnight. Services prices rose 0.22% 2w/2w, also in line with the previous data at 0.21%, with some pressure in other services, in items related to tourism, and housing. The non-core component decreased by 0.19% 2w/2w due to deflation in agricultural prices, for the ninth fortnight in a row, with relief in items such as onions and potatoes. We expect fresh food items to post some rebound during this year. Energy prices also decreased during the fortnight (-0.71%), mainly due to gasoline prices.

In annual terms, headline inflation decelerated to 3.67%, from 3.81% in the second half of February. Core CPI was down, from 3.66% in the previous month to 3.56% now, with merchandise at 2.92% (from 2.76%) and services at 4.25% (from 4.65%). In the February 6th statement, Banxico forecasted 3.7% for headline and 3.6% for core during the 1Q25, in line with data as of the 1H of March.

Our take: Today’s print reinforces our view that the disinflationary trend continues, supported by low agricultural prices and a slowdown in economic activity. However, the inflation outlook remains challenging, with the peso depreciation, volatile climate conditions including droughts in some parts of the country, and a tight labor market posing risks. We forecast CPI to end 2025 at 3.9%. Regarding the policy rate, we maintain our call for a 50bps rate cut on March 27th down to 9.0%, with a year-end forecast of 8.50%.