We expect the central bank of Mexico (Banxico) to cut its policy rate by 25-bp in the August 8 meeting (reaching a level of 10.75%) in a split decision. In our view, board members Irene Espinosa and Jonathan Heath, which have expressed concern about the inflationary outlook, will be the dissenter voters (calling for another hold). On the other hand, we think that the rest of the board members will vote for a 25-bp rate cut considering the following:

1. The forward guidance in June’s monetary policy statement suggests greater willingness to consider a rate cut in the next meeting (link to our monetary policy note). June’s forward guidance states: “Looking ahead, the Board foresees that the inflationary environment may allow for discussing reference rate adjustments.” The previous forward guidance mentioned: “Looking ahead, it will assess the inflationary environment in order to discuss reference rate adjustments.” The corresponding minutes suggest at least three board members (including deputy governor, Omar Mejía, who voted for a rate cut in June) are open for resuming rate cuts. Even one of the board members which had a hawkish tone in the minutes did not discard fine-tuning adjustments in the policy rate (Link to our monetary minutes note).

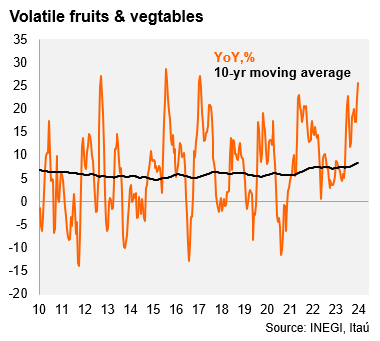

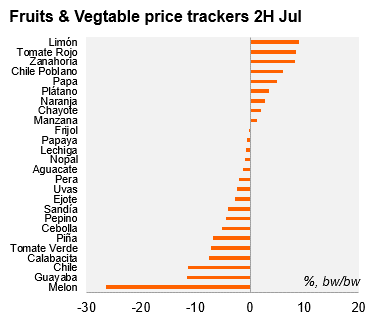

2. While headline inflation rebounded strongly (5.61% in 1H July), it is mainly due to the non-core index (10.64%) driven by volatile fruits & vegetables prices (25.69%) which pressure should revert to the mean relatively quickly (see left chart below). Our proprietary fruits & vegetables price trackers point to eased pressure in the 2H of July (0.26% bw/bw, relative to previous figures which were around 6%). We note the slight pressure in F&V prices in 2H July is not broad based, with red tomatoes exerting the most pressure (contribution to the F&V index of around 90-bp). We expect bi-weekly CPI to expand 0.15% in 2H of July (from 0.21% a year ago and 5-year median of 0.21%), while core inflation stood at 0.12% (from 0.09% a year ago and 5-year median of 0.09%). We note that the 2H July figure will be published under a new base (there is no information about the new base’s weights, in contrast to the previous change in 2018 when the preliminary weights were known a year in advance) which could be a slight challenge to the accuracy of our forecast.

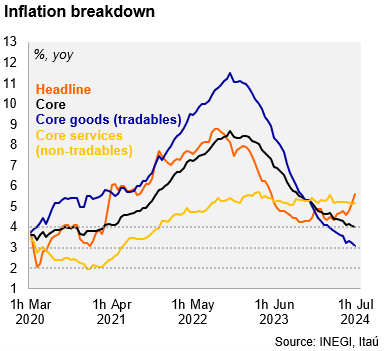

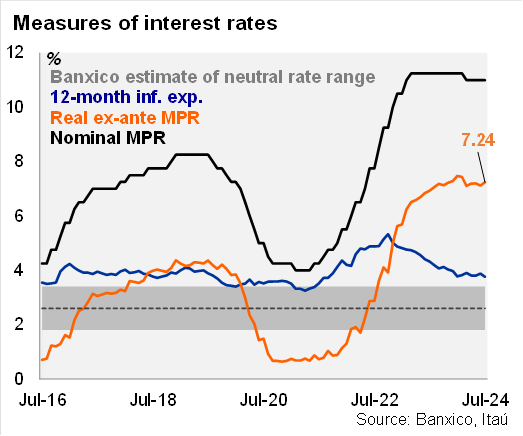

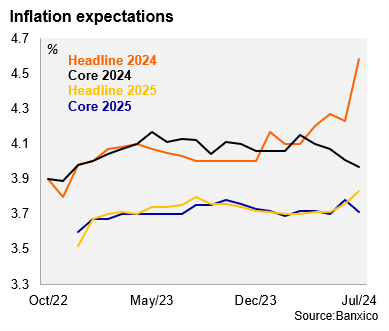

3. Core inflation continued to ease, although services inflation remains persistent. Core inflation stood at 4.02% YoY in 1H of July 2024, compared to the end of last year of 4.98% and its peak of 8.66% in 1H November 2022. On the other hand, twelve-month ahead inflation expectations (average) also fell to 3.76% in July (from 3.88% in June), taking the real ex-ante rate to 7.24% (previously at 7.12% and compared to the real neutral rate of 2.6%). The highly restrictive stance relative to the lower core inflationary gap suggests there is space for a rate cut, without abandoning a highly restrictive stance to ensure core inflation continues converging to the target. We also note that while headline inflation expectations for 2024 and 2025 rose, core inflation expectations fell (see chart below).

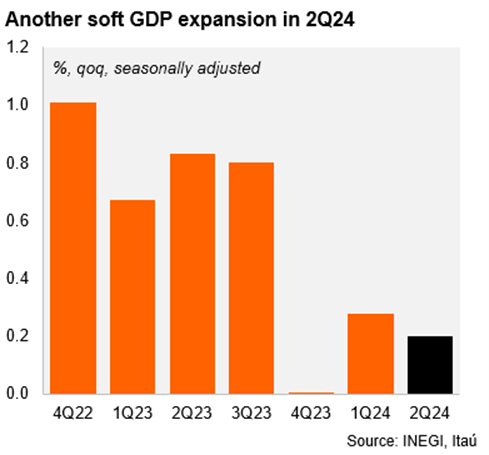

4. A weaker than expected activity outlook could make some board members more comfortable with services inflation beginning to trend down more clearly in the future. Despite strong fiscal expenditure in 1H24, GDP growth in 1Q24 was soft (0.3% qoq/sa) and the flash GDP estimate for the 2Q24 stood at 0.2%. Leading indicators of private consumption suggest it is slowing in the 2Q24 (private consumption in April fell by 0.9% MoM/SA, with the qoq/saar at 6.6% in April from 8.0% in 1Q24). Softer GDP in 2Q24 is one of the main reasons we reduced our GDP growth forecast for 2024 from 2.3% to 1.6%, in our most recent macro scenario. Activity in the 2H24 is unlikely to see a strong rebound as fiscal expenditure will likely soften.

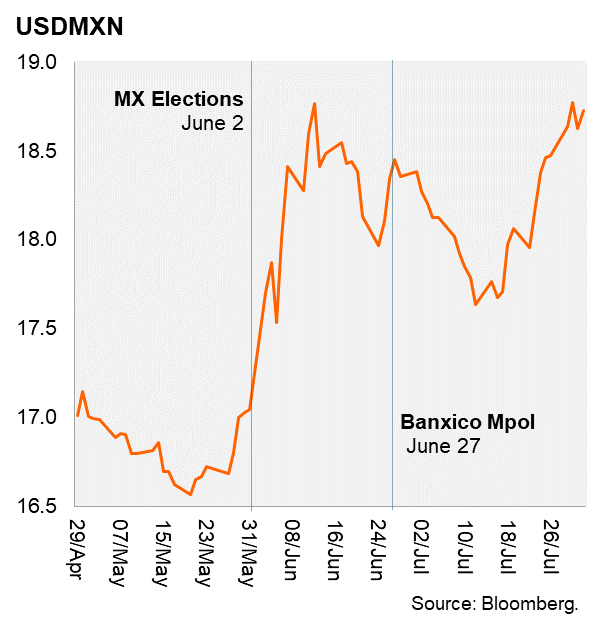

5. While the depreciation of the currency may play against cutting rates in August (a risk to our call), the USDMXN’s level is not that different to the one at June’s monetary policy meeting, and Banxico pass through estimates are relatively small (the elasticity coefficient of inflation to exchange rate is estimated at 0.04 over a 12-month horizon and 0.06 in the long term). Moreover, the Fed signaling a rate cut is on the table in the September meeting also supports Banxico reducing the policy rate.

Finally, we think that the monetary forward guidance will remain broadly unchanged, but probably their headline inflation forecast will be increased in the short term to reflect the temporary non-core fruits & vegetables inflation shock. Keeping the current forward guidance, “Looking ahead, the Board foresees that the inflationary environment may allow for discussing reference rate adjustments.”, would grant flexibility for another pause if necessary, considering that the discussion of the judicial reform in Mexico, and U.S. elections could generate volatility. Our base case remains for the central bank to cut its policy rate by 25 bps in each of the subsequent meetings of the year, reaching an end-of-year level of 10.00%. Certainly, bouts of volatility related to post-election uncertainty and U.S. elections risk another pause.