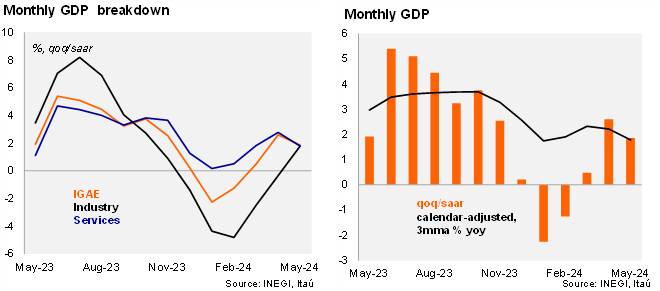

The monthly GDP proxy (IGAE) rose by 1.6% YoY in May, above market consensus (as per Bloomberg) and our call - both at 1.4%. Using calendar adjusted figures, IGAE expanded at a similar pace (1.5%), taking the quarterly annual rate to 1.8% in May (from 2.3% in 1Q24). Using seasonally adjusted figures, the monthly GDP proxy rebounded to 0.7% MoM/SA, after falling by 0.7% in April. The headline figure was supported by construction (2.5%) and services s (0.8%), while manufacturing production registered a practically null sequential expansion. Activity momentum improved in May, with the qoq/saar at 1.9% (from 0.5% in 1Q24).

Our take: The rebound in activity in May, after a weak April figure, is consistent with our call of a softer 2Q24 which was one of the main reasons we recently reduced our GDP growth forecast for 2024 to 1.6% (from 2.3%). Looking at the 2H24, fiscal expenditure is not projected to support activity (after elections and due to the transition of administrations), likely moderating growth rates in services and construction sectors. Manufacturing output, which has been relatively muted in 1H24, could rebound during the rest of the year amid a weaker currency. A softer activity outlook could lead Banxico board members to be more comfortable in resuming their easing cycle in the August meeting (and subsequent policy decisions). Our base scenario is for a 25-bp rate cut in the August 27 meeting, with cuts of the same magnitude in each of the policy meetings of the rest of the year (end of year policy rate forecast at 10.00%). The risk to our call is further bouts of market volatility from the new political landscape and/or U.S. election.

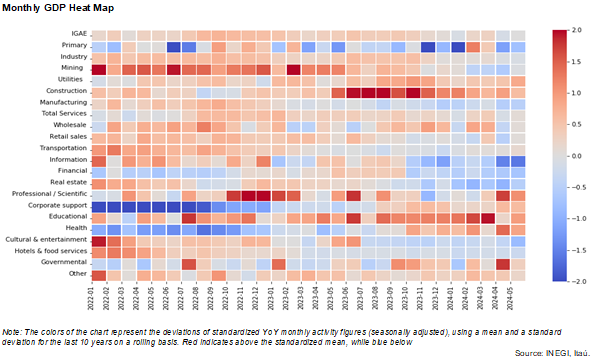

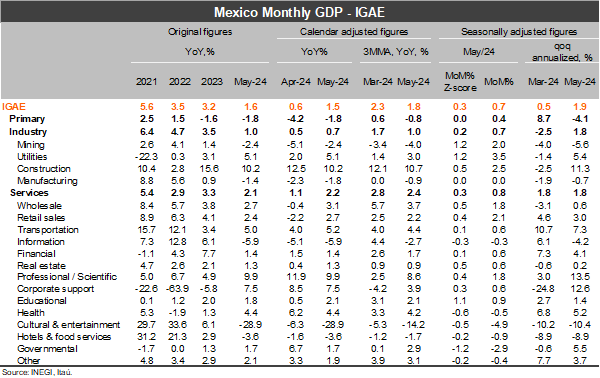

See detailed data below