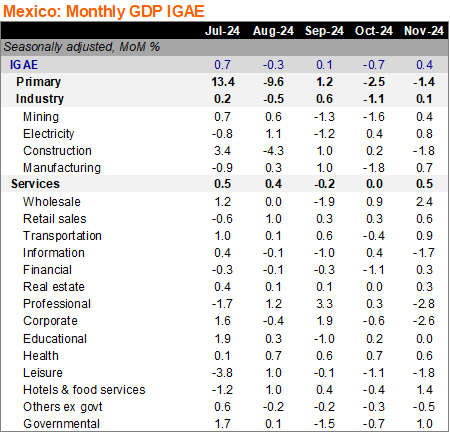

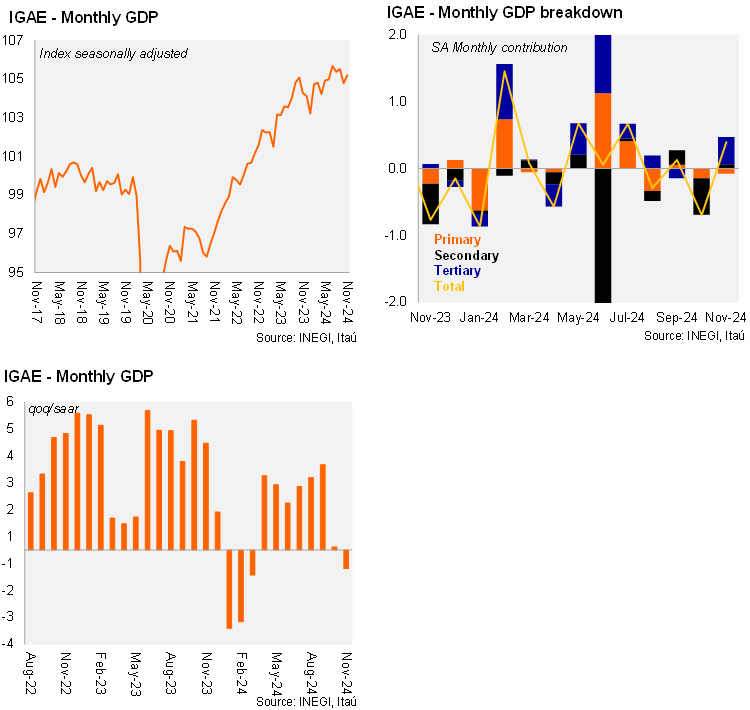

Economic activity rose 0.53% YoY in November, between Bloomberg’s market consensus (0.70%) and our forecast (0.0%). By sectors, services grew 1.60%, with 8 out of 14 subsectors up supported by solid fundamentals. Industry fell by 1.40% YoY, mainly explained by mining and construction, partly on a negative base effect. Agricultural remained somewhat weak at 0.20%, after a large contraction of 4.82% in October. Using seasonal adjusted figures, the economy rose by 0.40% MoM, higher than both consensus (0.25%) and our forecast (0.15%), which is a modest rebound after the contraction in October (-0.69%). Services were up 0.48% MoM, mainly driven by wholesale, retail and leisure activities. On the other hand, the industrial sector increased 0.14% MoM, not offsetting the fall of the previous month (-1.12%). Primary activities decreased 1.36% MoM, adding two months of contractions.

Our view: Today’s figures showed a modest rebound during November that couldn’t offset October’s performance. As a result, the QoQ SAAR stood at -0.7% (from +0.1% in the previous quarter). For GDP, we expect an increase of 1.2% YoY in the 4Q24 (from 1.7% YoY in 3Q24). In sequential terms, we forecast a contraction of 0.1% QoQ and -0.5% QoQ SAAR. This is consistent with a full year increase of 1.6% YoY (from 3.3% YoY in 2023).

See details below