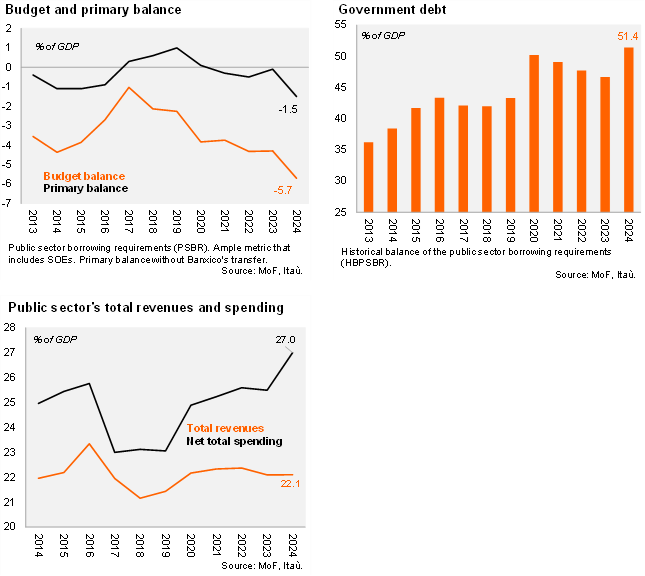

The result was mainly explained by an increase in total real expenditures of 7.7% YoY, due to the finalization of infrastructure projects and a high financial cost. Regarding income, the slight growth of 1.7% YoY in real terms was supported by higher-than-expected import tax and income tax revenues, despite the deep contraction of oil revenues in a context of decreasing oil production and lower than projected gas prices. Finally, net government debt came in at 51.4% of GDP, in line with our forecast and the MoF’s.

Our view: Fiscal accounts remained in a challenging spot during 2024 with high expenditures and a drag from oil revenues, despite the efficient measures to raise income-related revenues. For 2025, we anticipate a fiscal consolidation with a nominal deficit of 3.9%, as well as a contained net government debt of 51.8% and a positive primary balance of 0.6% in a context of lower interest rates than the previous year. We think that despite some tailwinds for revenue in 2025, more aggressive measures would be needed in 2026.