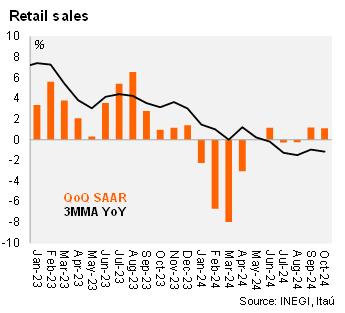

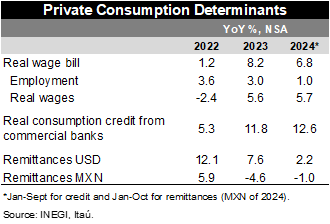

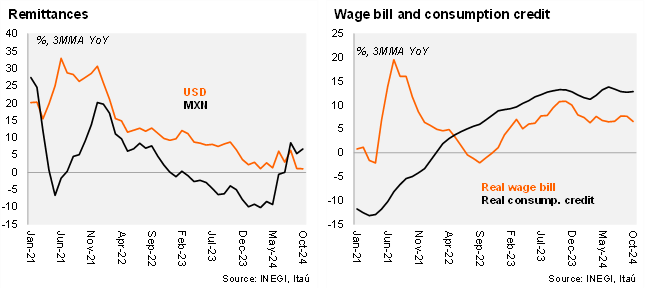

Retail sales fell by 1.2% YoY in October, slightly below market expectations of -1.0% (as per Bloomberg). In seasonally adjusted terms, retail sales were down 0.3%, mainly impacted by negative results in household goods and motor vehicles. Supermarkets, on the other hand, were up 1.5% compared to September. Most private consumption determinants remain supportive, with the YTD of the real wage bill at 6.8% in October, while real consumption credit from commercial banks and remittances in MXN stood at 12.6% and -1.0%, respectively. During this year, many items, such as clothes and footwear, were affected by international competition with lower prices, which affected national production and sales, especially in Guanajuato region, the most important producer of textiles and leather in Mexico.

Our take: Today’s retail sales data add to the recent releases, namely industrial production, CPI, private consumption, investments, among others, that surprised to the downside since the last Banxico meeting. We expect a 50bps cut at the last monetary policy decision of the year given the benign inflation scenario at the margin, as well as the well-behaved USDMXN. Our GDP growth forecast for 2024 stands at 1.7% (+1.4% YoY 4Q24). For 2025 we forecast 1.5%.

See detailed data below