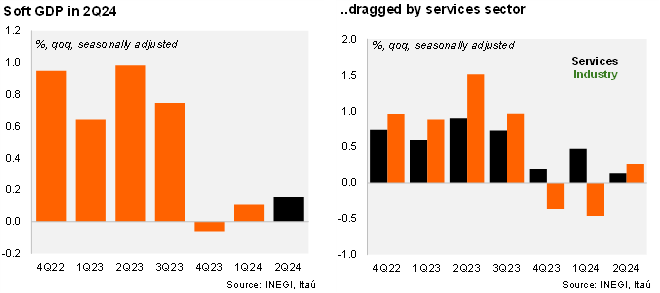

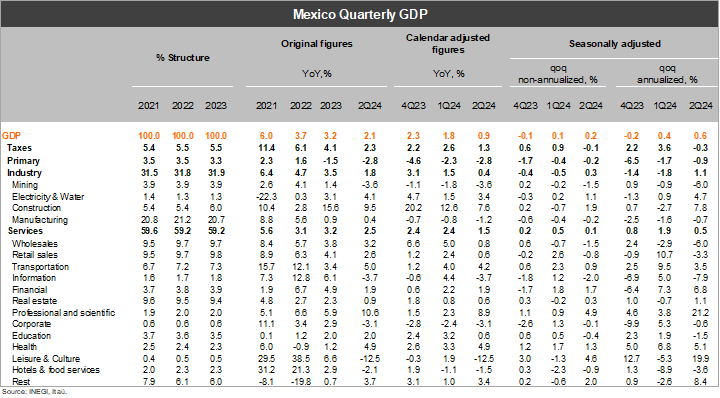

GDP in 2Q24 rose by 2.1% YoY, slightly below our forecast and market consensus (as per Bloomberg) – both at 2.2%. The headline figure was boosted by a favorable calendar base effect (Easter Holidays). In fact, GDP only expanded by 0.9% YoY adjusted by calendar effects. Using seasonally adjusted figures, GDP expanded at a soft 0.2% QoQ/SA in 2Q24, dragged by a soft services sector (0.1%). Industrial production expanded 0.3% QoQ/SA supported by construction output (1.9%) but with a weak manufacturing production (-0.2%). Finally, primary production fell by 0.2%.

Our take: Our GDP growth forecast of 1.6% has a downside bias. Of note, we began the year forecasting 2024 GDP growth at 2.8%, which was revised down to 2.3% in May, mainly due to weaker data in 1Q24. Persistent underperformance of economic activity and a slight revision to our growth outlook in the US led us to downshift our growth call in July to 1.6% and to 1.7% for 2025 (from 1.9%). Activity is unlikely to pick up significantly during the rest of the year considering an expected retrenchment of fiscal spending and softening of the U.S. economy. The depreciation of the currency could give some support to activity through the manufacturing sector and remittances (as a determinant of private consumption), but we think it is not enough to change the downside bias. A weak activity outlook amid a lower core inflation gap (vs. a very restrictive monetary stance) and higher odds of the Fed starting its easing cycle in September will likely lead most Banxico members to push for further rate cuts of 25-bp in each of the remaining meetings of the year (our end of year policy rate forecast is at 10.00%).