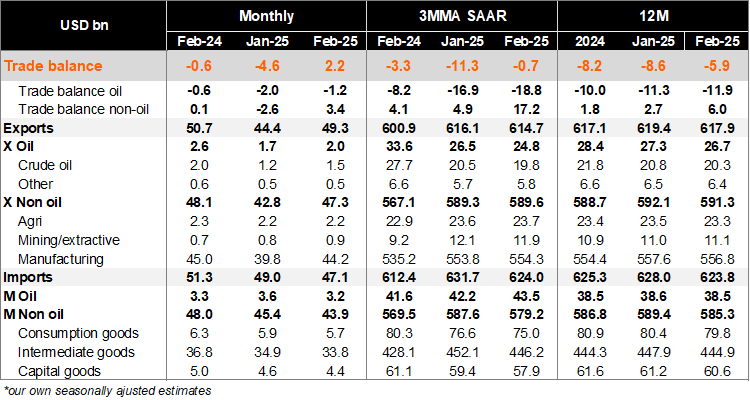

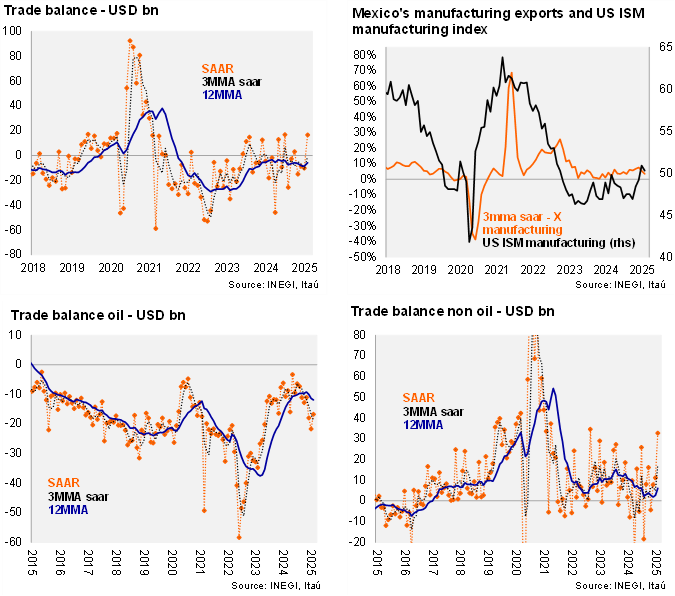

The trade balance in February revealed a USD 2.2 billion surplus, above the Bloomberg’s market consensus of a USD 527 million deficit. As a result, on a 12-month rolling basis, the trade deficit reached USD 5.9 bn, down from USD 8.6 bn in January (USD 8.2 bn in 2024). At the margin, using three-month annualized seasonally adjusted figures, the trade balance improved to close to zero (USD 700 mm deficit), a significant swing from the USD 11.3 bn deficit in the previous month. Looking at the breakdown, the oil trade balance deficit continued to deteriorate at the margin (USD 18.8 bn deficit vs USD 17.2 bn surplus for non-oil) following the decline in domestic oil production and the government’s strategy to prioritize domestic oil refineries.

Our view: the better-than-expected result in the trade balance in February is a result of lower imports, in line with the deceleration of the domestic economic activity since the last quarter of 2024. Exports, on the other hand, remain at solid levels, still no clear sign of disruption given tariff discussions. The uncertainty surrounding Mexico’s trade relationship with the US will remain a challenge for trade flows. Looking ahead, the performance of oil exports will be influenced by domestic policies towards national sovereignty. Weaker internal demand and a slowdown in construction are likely to limit non-energy consumption and capital imports, particularly for non-residential projects.

See detailed data below