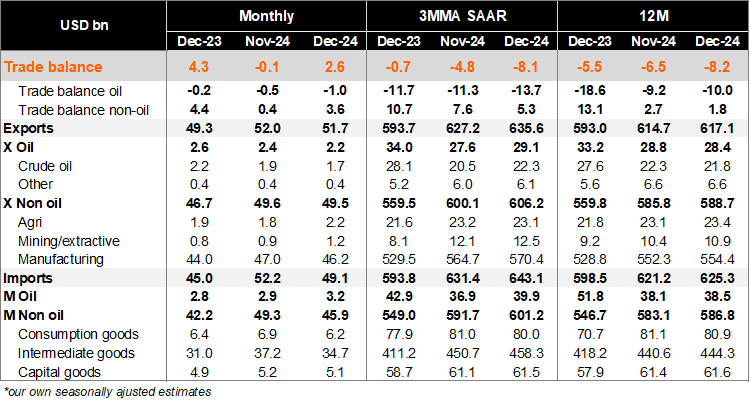

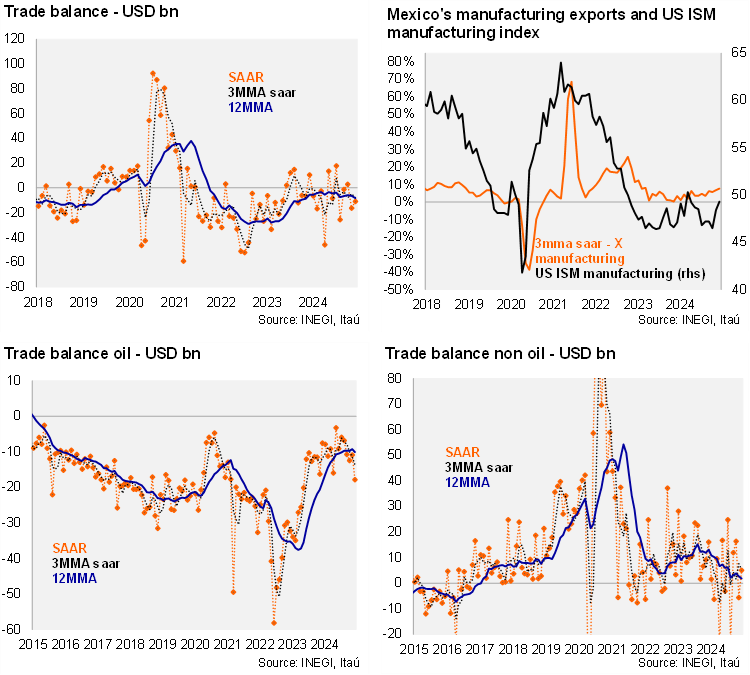

The trade balance in December revealed a USD 2.6 billion surplus, close to Bloomberg’s market consensus of USD 2.7 billion. As a result, the trade deficit reached USD 8.2 billion in 2024 (from a deficit of USD 6.5 billion on a 12-month rolling basis in November and a deficit of USD 5.5 billion in 2023). At the margin, using three-month annualized seasonally adjusted figures, the trade balance stood at a deficit of USD 8.1 billion in December. Looking at the breakdown, the oil trade balance deficit continued to deteriorate at the margin (USD 13.7 billion deficit vs USD 5.3 billion surplus for non-oil) following the decline in oil production and the government strategy to prioritize domestic oil refinery.

Our view: A weaker currency along with expectations of outperformance of the U.S. economy should continue to support manufacturing exports during the next months. Weaker internal demand and a deceleration of construction should curb non-energy consumption and capital imports used mainly for non-residential edification. Institutional uncertainties and tariff threats should impact trade flows. Also, on the domestic front, the trade balance will be influenced by the recent presidential decree on the textile industry (35% tariffs on finished products and 15% tariffs on textiles), and a differentiated tax rate for marketplaces from countries without a trade agreement with Mexico.

See detailed data below