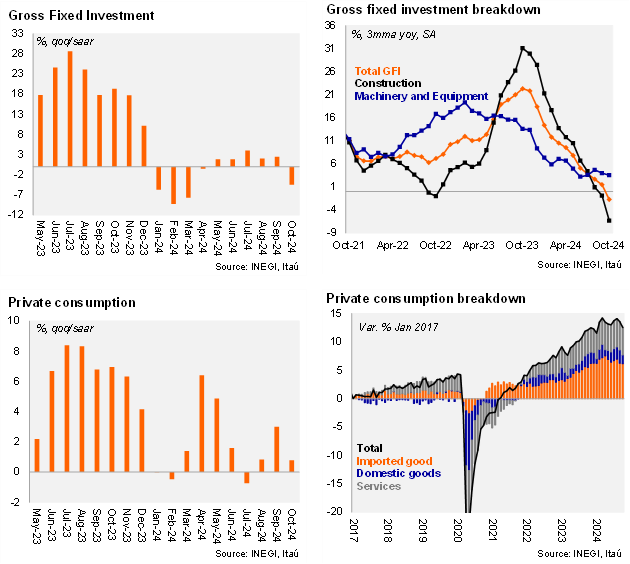

Gross Fixed Investment (GFI) fell by 2.6% YoY in October, a slightly smaller contraction compared to Bloomberg’s consensus of 2.8%. By sectors, machinery and equipment increased 7.8%, with both imported and national aggregations up. Construction, however, fell further (-11.0% YoY) with public and non-residential components down. Using seasonally adjusted data, investment rose only 0.1% MoM, in line with market expectations. Machinery and equipment increased 1.2% MoM, while construction declined 0.9%, with non-residential as a drag (-2.4%) due to the finalization of public infrastructure projects.

Private consumption stood at 1.4% YoY, also in line with consensus. On a monthly basis, private consumption decreased 0.7%, down for two months in a row, with declines in services (-0.3%), domestic goods (-1.5%) and imported goods (-0.5%). In addition, INEGI released its nowcast for November and December for private consumption at +0.6% and +0.1% MoM, respectively.

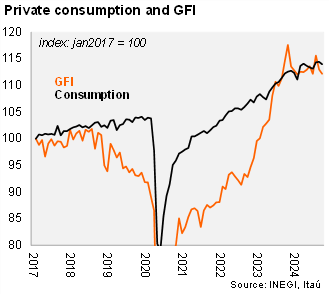

Our view: October domestic demand figures showed mixed results for the start of 4Q24, with investment down 4.5% QoQ/SAAR, while consumption up 0.8%. We expect consumption to remain the key driver of domestic demand in 4Q24, while investment faces risk due to external factors, domestic uncertainties, and a high base effect. We expect domestic demand to slow its pace during the following months. We forecast GDP to grow 1.4% YoY in 4Q24 and 1.7% for the year-end.