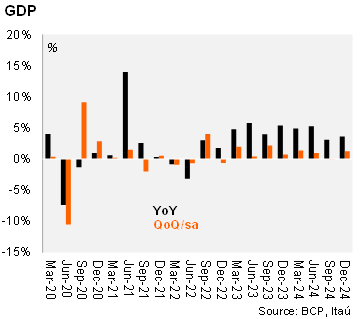

GDP expanded by 3.6% in 4Q24, up from 3.1% in 3Q24. Looking at the breakdown on the supply side, the annual print was influenced by the positive performances in construction (+13.6% yoy), services (4.8% yoy), manufacturing (3.1% yoy), livestock, forestry and fishing (+2.7% yoy). On the other hand, the electricity sector fell by 7.9 % yoy affected by the low level of the Paraná river and agriculture decreased 4.3% yoy in 4Q2, affected by a drought. Thus, in 2024, GDP expanded at a solid 4.2%, down slightly from the 5.0% growth in 2023. At the margin, using our seasonally adjusted series, GDP rose sequentially in 4Q24 (1.3% qoq/sa), leaving the statistical carryover for 2025 at 1.2%.

Domestic demand improved in 4Q24. Internal demand increased by 9.9% year over year in 4Q24 (from 5.9% in 3Q24) driven by total consumption (private 6.4% yoy and public 5.7% yoy), which continues its expansionary path, growing by 6.3% yoy (from 4.7% in 3Q24), while gross fixed capital formation expanded 13.3% yoy (from 8.0% in 3Q24) driven by construction, machinery and equipment sectors. On the external side, exports of goods and services fell by 16.0% (from -6.2% in 3Q24), due to lower sales of soybean and electricity. Moreover, the imports of goods and services declined by 0.1% (from -0.6% in 3Q24) due to a contraction of machinery and equipment and chemical products.

Our take: Our 2025 GDP growth forecast remains at 3.5%, with downside risk due to the drought and despite the positive carryover. On the demand side, we expect private consumption to continue supporting growth helped by the spillovers from Argentina.