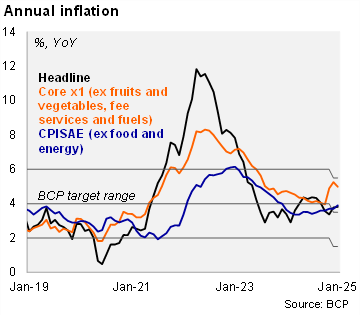

CPI rose by 1.0% MoM in January (from 0.9% a year ago), above our forecast (0.7%) and market consensus (0.5%), according to the BCP survey. The month's outcome was mainly explained by increases in most of the groups of the basket, with food and services standing out. In particular, vegetables and legumes (24.4% MoM) had the largest impact on monthly inflation. There were also increases in meat products, including beef and substitutes such as pork and poultry. Furthermore, prices of imported durable goods rose (0.5% MoM), due to a weaker PYG. Core CPI x1 (excludes fruits and vegetables, regulated service prices and fuel) increased by 0.6% (from 0.9% a year ago), due to higher meat prices (1.3% MoM). On an annual basis, headline inflation rose to 3.8% in January (same figures in December 2024), while the core X1 CPI fell to 5.0% from 5.3%. We note that both the headline and the core remain within the tolerance band of the BCP’s new inflation target (3.5% +/- 2%).

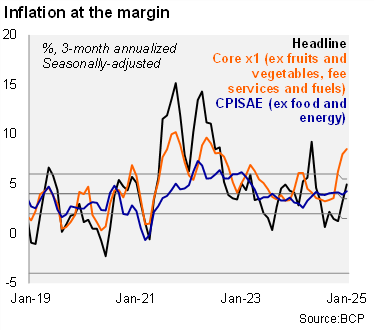

At the margin, both the headline and the core inflation accelerated in January. Using our own seasonally adjusted figures, the three-month annualized headline inflation reading rose to 4.9% in January (from 3.2% in December), while core inflation hit 8.5% (from 8.0% in the previous month).

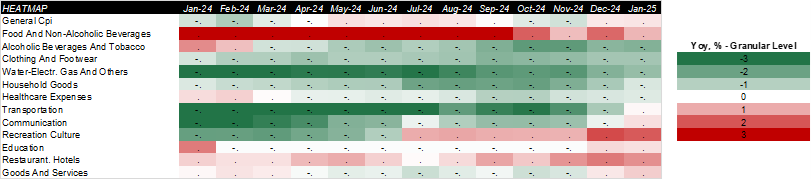

Despite the greater-than-expected inflation print in January, our heat map shows that 42% of the items are below the central bank's revised inflation target of 3.5%, is lower than the end-2024 data (58%).

Our take: We forecast inflation at 3.5% by the end of 2025, in line with the middle of the central bank's target. Regarding monetary policy, a lower inflation target and our expectation that the Federal Reserve will not cut rates this year limits the scope for further easing in 2025. The next monthly monetary policy meeting will be held on February 21, while the CPI for February will see the light on March 3.