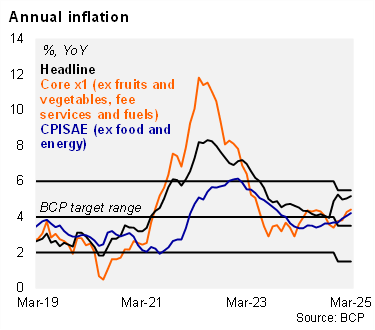

CPI rose by 1.2% MoM in March (from 1.1% a year ago), well above our forecast (0.3%) and market consensus (0.4%), according to the BCP survey. Inflation dynamics in the month were mainly characterized by price increases in the food basket, especially fruit and vegetable products, increases in durable goods of imported origin, which were partly offset by the decline in fuel prices. In particular, volatile fruit and vegetables prices rose by 20.6% MoM. In addition, imported consumer goods (excluding fruits and vegetables) increased by 0.3% MoM, partly due to the depreciation of the Guarani against the US dollar. On the other hand, fuel prices fell by 0.8% MoM, driven by downward adjustments in gasoline. The Core CPI x1 (excludes fruits and vegetables, regulated service prices and fuel) increased by 0.5% (from 0.4% a year ago). On an annual basis, headline inflation rose to 4.4% in March (up from 4.3% in February), while the core X1 CPI stood at 5.2%. We note that both the headline and the core remain within the tolerance band of the BCP’s inflation target (3.5% +/- 2%).

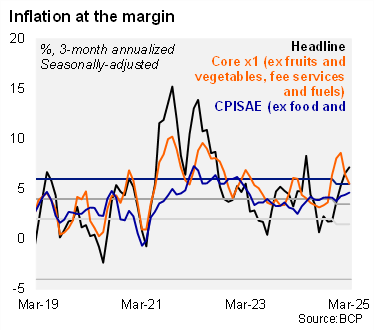

At the margin, headline inflation accelerated, while core inflation decelerated in March. Using our own seasonally adjusted figures, the three-month annualized headline inflation reading rose to 7.2% in March (from 6.6% in February), while core inflation fell to 5.5% (from 6.5% in the previous month).

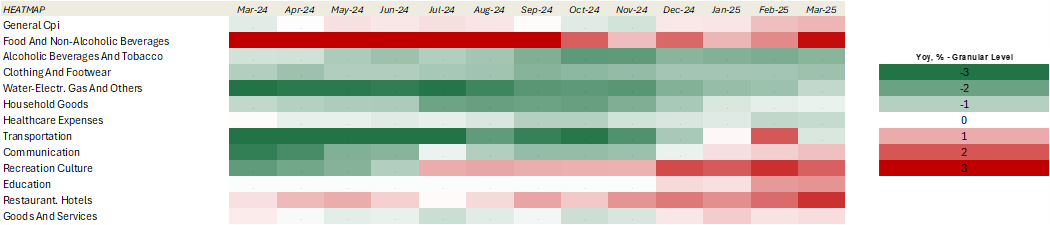

Our heat map shows that 50% of the items are below the central bank's inflation target of 3.5%, which is lower than the end-2024 data (58%).

Our heat map shows that 50% of the items are below the central bank's inflation target of 3.5%, which is lower than the end-2024 data (58%).

Our take: Our YE25 inflation forecast stands at 3.5%, in line with the center of BCP’s target range, but the persistence of volatile prices introduces upside risks to our call. Regarding monetary policy, higher-than-expected CPI and our expectation that the Federal Reserve will not cut rates this year limits the scope for further easing in 2025. The next monthly monetary policy meeting will be held on April 23, while the CPI for April will see the light on May 2.

Andrés Pérez M., Diego Ciongo & Soledad Castagna