Monthly real GDP increased by 3.9% YoY in November, above our 3.4% call and market consensus (3.2%) (3.4% YoY in October).

Primary activities benefited from a strong expansion in agriculture (+12.4% YoY in November), fishing (+18.0% YoY in November), partially offset by mining (-2.2% YoY in November).

Secondary activities were positive. Manufacturing rose 6.7 % YoY in November, up from 1.7% YoY in October. Commerce rose 3.5% YoY (3.8% YoY in October), while Hotels and Restaurants grew by 4.8% YoY in November (4% in October), both benefited by withdrawals from pension funds and the recovery of real wages. Transportation increased 8% YoY in November. In contrast, construction contracted 2.4% YoY in November (4.8% in October).

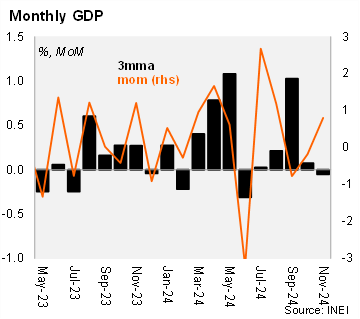

Activity momentum remained positive but decelerating. Using unofficial seasonally adjusted series, the monthly GDP rose by 0.8% MoM/SA in November (after fell 0.2 MoM/SA in October). The carryover for 4Q2024 is tracking at 0.6% QoQ sa from 1% QoQ sa in Q32024.

Our take: The activity recovery remains well on track. Most business confidence indicators remain in positive territory, while imports of capital goods rose by 10% in October. We expect GDP growth at 2.9% in 2024 and 2.8% in 2025, slightly below potential of 3.0%. The execution of mining and infrastructure projects, along with the increase in consumption in the context of the recovery of real incomes will drive growth this year. Activity will likely face headwinds from the bouts of strikes related to security concerns and the high political uncertainty. In addition, a renewed US-China trade war poses downside risks to Peru’s growth outlook for 2025 and beyond, through a weaker external impulse and lower terms of trade. One third of Peru’s exports are destined to China.