In its monthly monetary policy meeting held in April, the Central Reserve Bank of Peru (BCRP) held its benchmark interest rate steady at 4.75% again, in line with both market consensus and our expectations. The policy rate has been at 4.75% since January. The BCRP’s communiqué highlights the deterioration in the global economic outlook due to rising policy uncertainty and trade tensions, and the rise in inflation expectations across several economies, including the US. In this context, the BCRP acknowledged ongoing volatility in global financial markets and a deterioration in global growth prospects. Domestically, however, recent hard data suggested that Peru’s economic activity was gaining traction in recent months, with output expanding near potential.

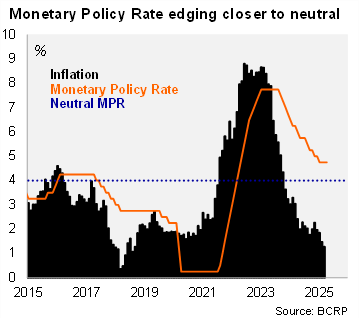

Headline inflation has been within the target range (2+/-1%) for twelve consecutive months, and core inflation has been in the range since August. Headline and core inflation stood at 1.28% and 1.9% in March, respectively. Twelve-month inflation expectations remain at 2.28% in March, which would take the one year real ex-ante rate at 2.47%, edging closer to the 2.0% neutral real rate.

Our take: The deterioration of the global outlook, in the context of well-behaved inflation and inflation expectations, set the stage for further cuts down the road. In the short term, we anticipate a moderation in inflation in April, although upward risks remain due to persistent food supply constraints. We expect headline inflation to rebound in upcoming months, reflecting adverse base effects. Our forecast for the end of 2025 stands at 2.3%, somewhat above the Central Bank’s estimates. For 2026, weaker domestic demand, along with lower oil prices, should lead to a swifter disinflation path. Given subdued inflation dynamic and deteriorating external conditions, we expect the BCRP will be inclined to cautiously resume its easing cycle later this year, edging further towards neutral. The next monthly monetary policy meeting is scheduled for May 8.