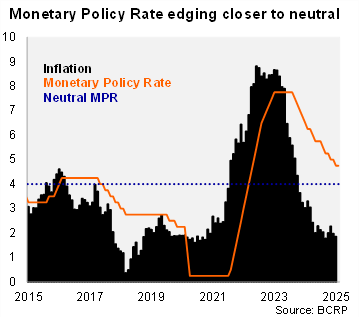

In its February meeting, the Central Bank of Peru (BCRP) maintained the policy rate at 4.75%. The decision was in line with our call and with the Bloomberg median, although a sizable share has called for a cut. The communiqué removed the wording from the January meeting that the policy rate is near neutral levels. The statement repeated the data dependent guidance, keeping the door open for further rate adjustments depending on inflation (emphasizing the core index) and its determinants, inflation expectations, and activity. The BCRP has eased by a total of 300bp (peak at 7.75%) throughout the easing cycle that began in September 2023.

Headline inflation has been within the target range (2+/-1%) for ten consecutive months, and core inflation is in the range since August. Headline and core inflation stood at 1.85% and 2.4% in January, respectively. The central bank expects annual inflation to approach the lower limit of the target range in the coming months and then return to the midpoint of the target. Twelve-month inflation expectations fell to 2.37% in January, from 2.5% in December, which would take the one year real ex-ante rate at 2.38%, edging closer to the 2.0% neutral real rate.

Out Take: We expect inflation to remain within the BCRP’s inflation target range through 2025, with activity around its potential level of 3%. That said, the 10% nominal minimum wage hike poses an upside risk to inflation, while base effects from last year’s downside inflation surprises could lead to transitory bumps in the inflation path towards the end of the year. We believe that the BCRP is likely to cautiously deliver a final rate cut in the easing cycle this year, from the current 4.75% to 4.5%. The next monthly monetary policy meeting will take place on March 13.