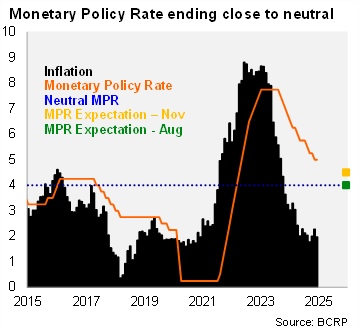

In its January meeting, the Central Bank of Peru (BCRP) lowered the policy rate to 4.75%. The market was deeply divided with a slim majority opting for a cut, while we saw reason to continue to hold rates. The communiqué re-introduced wording from the November meeting (5%) that the policy rate is near neutral levels. Inflation at the center of the target range, expectations remaining within the target range, and a softening activity outlook at the margin were justifications to lower rates. The statement repeated the data dependent guidance, keeping the door open for further rate adjustments depending on inflation (emphasizing the core index) and its determinants, inflation expectations, and activity. The BCRP has eased by a total of 300bp (peak at 7.75%) throughout the easing cycle that began in September 2023.

Headline inflation has been within the target range (2+/-1%) for nine consecutive months, and core inflation is in the range since August. Headline and core inflation stood at 2% and 2.6% in December, respectively. The central bank expects annual inflation to remain in the target range in the forecast horizon. Twelve-month inflation expectations remained slightly below 2.5% in December, which would take the one year real ex-ante rate to roughly above 2.25%, edging closer to the 2.0% neutral real rate.

Out Take: With inflation expected to remain in the target range over the policy horizon, activity around the potential level, we expect the policy rate to continue to approach neutral. However, the BCRP is likely to move cautiously in the context of fewer cuts by the Fed and a tighter global financial condition. The next meeting will take place on February 13.