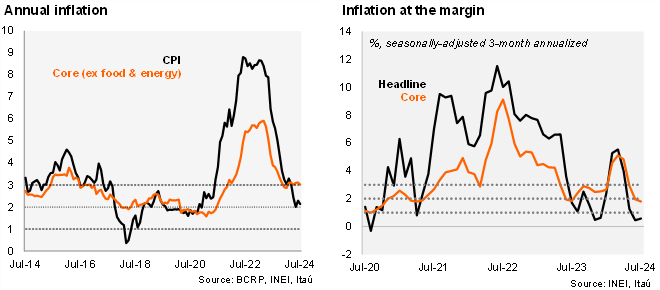

CPI increased 0.24% MoM in July (from 0.39% a year ago), above our forecast of 0.45% and market expectations of 0.40% (as per Bloomberg). Food (contribution of 8-bp) and transportation (contribution of 8-bp) subindexes exerted the most upside pressure to the headline figure. The latter reflects seasonal factors due to national holidays. Core inflation (excluding energy and food items) stood at 0.19% MoM (from 0.29% a year ago). On an annual basis, headline inflation fell to 2.13% YoY in July (from 2.29% in June), still within the central bank's target range (2+/-1%), while core inflation fell slightly to 3.01% (from 3.12%). At the margin, the seasonally adjusted three-month annualized CPI came in at 0.58% in July (from 0.45% in June), while core inflation stood at 1.80% (from 1.96%).

Our take: While headline inflation remains well-behaved, core inflation remains persistently around the upper bound target of the central bank (BCRP) since the beginning of the year. Given the emphasis that the BCRP statements have given to core inflation (“The Board is particularly attentive to new information on inflation and its determinants, including the evolution of core inflation [..] to consider, if necessary, additional changes in the monetary stance.”), we believe that the central bank will extend the pause at 5.75% in the August meeting despite below trend economic activity (although recovering) and headline inflation within the target range for four consecutive months. Still, we expect the BCRP will resume cuts during the rest of the year once core inflation eases more clearly towards the target (our end of year policy rate forecast is at 5.00%).