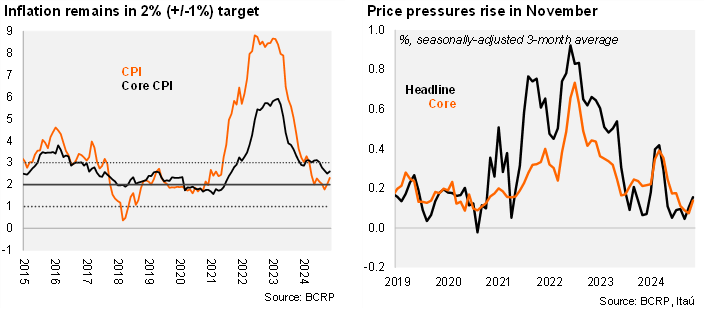

Inflation rose by 0.1% MoM in November, in line with market expectations and our call, and recovering from two consecutive falls. The monthly increase in November was mainly driven by consumption divisions, such as, Accommodation, Water, Electricity, Gas and Other Fuels, which had an increase of 0.47% MoM, Restaurants and Hotels that rose 0.11% MoM and Miscellaneous Goods and Services that advanced 0.26% MoM, which together contributed 86% of the variation of the general index. Otherwise, the Transportation division fell at the margin by 0.2% MoM. On an annual basis, inflation rose by 24 bp to 2.3%, given negative base effects, returning to the mid-point of the 2% (+/- 1%) target. Headline inflation has stood within the target range for eight consecutive months. Core inflation (ex-food & energy) rose slightly 0.06% in November, which led to an annual rose to 2.6% from 2.5% in October.

Out Take: We expect inflation to end the year at 2.6% YoY, and to decline slightly to 2.5% YoY by December 2025. In this context, we believe the BCRP is likely to pause in December. For 2025, fewer cuts by the Fed and still above target inflation expectations have led us to raise our terminal rate forecast to 4.5%, from 4.0%.