Inflation rose by 0.81% mom in March, above the historical variation of 0.7% recorded in March. The market was broadly divided with forecasts ranging from 0.3% to 1% mom. The monthly increase was mainly driven by Food and Alcoholic Beverage (1.85% mom; contributing 0.45% to the monthly variation), owing to a heat wave that affected the production of some foods, and education due to a seasonal effect (3.4% mom; contributing 0.3% to the monthly variation). Transportation fell 0.3% mom (contributing -0.03%). The other categories contributed less than 0.1% to the monthly variation.

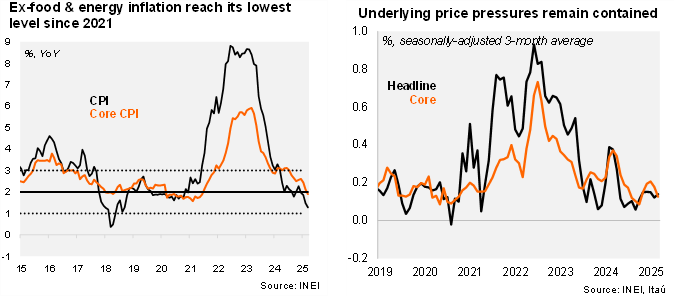

On an annual basis, despite the upside surprise in the month, inflation dropped by 20 bp to 1.28%, edging further towards the lower bound of the BCP’s 2% (+/- 1%) target. The BCRP warned that inflation would approach the lower limit of the target range in March due to base effects. Headline inflation has stood within the target range for twelve consecutive months. Core inflation (ex-food & energy) rose 0.64% in March, in line with the historical variation, which led to 1.9% YoY, its lowest level since 2Q2021.

Out take: We expect inflation to remain within the BCRP’s inflation target range through 2025, with activity around its potential level of 3%. We believe that the BCRP is likely to hold its monetary policy rate at 4.75% this year amid a challenging external scenario and high trade uncertainty. Still, we believe risks are skewed towards an additional 25-bp cut, taking the monetary policy rate to 4.5%.