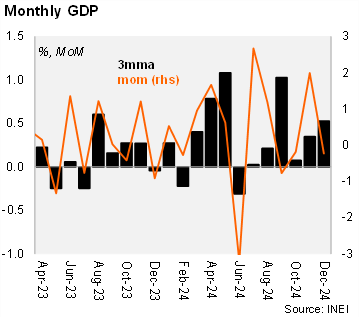

The monthly real GDP proxy increased by 4.9% YoY in December, above our call and market consensus (4%). Primary activities benefited from a strong expansion in agriculture (+7.5%), fishing (+76% YoY) and mining (2% YoY in). Secondary activities were positive. Manufacturing rose 11.85 % YoY in December, up from 7% YoY in November. Commerce rose 3.6% YoY (3.5% YoY in November), while Hotels and Restaurants grew by 4.5% YoY in December (4.8% in November), both benefited by withdrawals from pension funds and the recovery of real wages. Transportation rose 7.3% YoY (8% YoY in November). In contrast, construction contracted 1% YoY (-2.8% in November).

Activity momentum remained positive but decelerated. Using INEI’s seasonally adjusted series, the monthly GDP fell by 0.23% MoM/SA in December (after rising by 2% MoM/SA in November); 4Q2024 variation is tracking at 0.9% qoq sa (3Q24: 1% qoq sa).

Our take: The recovery in activity is on track. Most business confidence indicators remain in positive territory. Capital goods imports rose by 9% in 2024, due to expectations of a recovery in private investment. Overall, stronger activity at the backend of 2024, is projected to have increased GDP by 3.3% in 2024, above our call and the BCRP forecast (3.2%), also reflecting base effects from fishing (absence of significant weather shocks in 2024) among others. For now, we forecast GDP growth of 2.8% for 2025. Mining and infrastructure projects are expected to support growth on the supply side, while the recovery in real income and employment, as well as lower borrowing costs, are likely to put a floor on private consumption growth. However, a renewed trade war poses downside risks to the growth outlook for Peru.