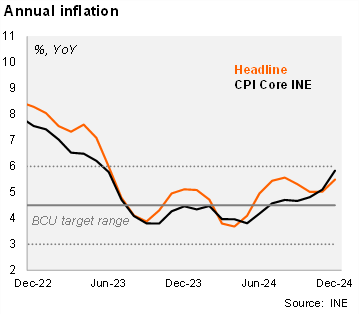

Headline inflation rose by 0.34% MoM in December (from -0.11% a year ago and a 5-year median figure of -0.14%). The print was slightly above our forecast (0.3%) and above market expectations according to the BCU’s survey (0.2%). The main monthly impacts came from recreation, sports and culture, which increased by 3.07% mom (incidence 0.17 p.p.), food and non-alcoholic beverages, which increased by 0.33% mom (incidence 0.09 p.p.), driven by higher meat prices. In addition, transport rose by 0.82% mom (incidence: 0.09 p.p.), and hotels and restaurants rose by 1.03% (incidence: 0.09 p.p.). On the other hand, housing, electricity, water fell by 1.45% MoM (incidence of -0.19 p.p.), mainly explained by the effect of the application of the "UTE rewards" program on the electricity supply bill. Core inflation (excluding fruits & vegetables and fuel prices) increased by 0.51% MoM, from -0.18% MoM in December 2023. On an annual basis, headline inflation rose to 5.49% (from 5.03% in November), while core inflation increased to 5.83% from 5.10% in the previous month. We note that despite the increase, both readings remain within the Central Bank's inflation target of 4.5% +/- 1.5%.

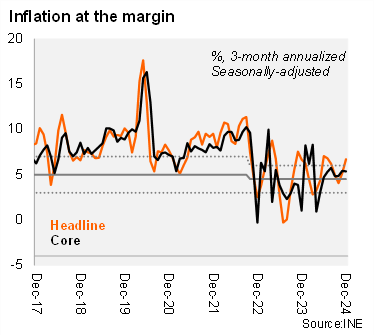

At the margin, headline inflation accelerated in December while core remained stable. Using our own seasonally adjusted figures, the three-month annualized headline inflation rose to 6.7% in December (from 5.1% in November), while core inflation was 5.4% (the same as in the previous month).

Our CPI heatmap shows that 15% of selected items are below the center of the central bank’s target (4.5%), worse than the previous month (38%) and the end of 2023 (38%).