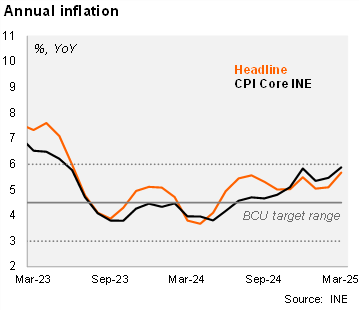

Headline inflation rose by 0.57% MoM in March (from 0.02% a year ago and a 5-year median figure of 0.80%). The print was above our forecast and market expectations according to the BCU’s survey (both at 0.5% MoM). The main monthly impact came from the food basket (1.8% MoM, incidence of 0.47 p.p.) driven by volatile fruits and legumes (9.8% MoM). Education services increased by 2.6% MoM (incidence of 0.1 p.p.), reflecting the annual adjustment of scholarship. On the other hand, restaurant and hotels prices fell by 0.53% MoM due to the end of the tourism holidays season. Core inflation (excluding fruits & vegetables and fuel prices) increased by 0.35% MoM, from -0.04% MoM in March 2024. On an annual basis, headline inflation rose to 5.67% in March (from 5.10% in February), while core inflation accelerated to 5.88% from 5.46% in the previous month. Despite some acceleration in the margin, both readings remain within the Central Bank's inflation target of 4.5% +/- 1.5%.

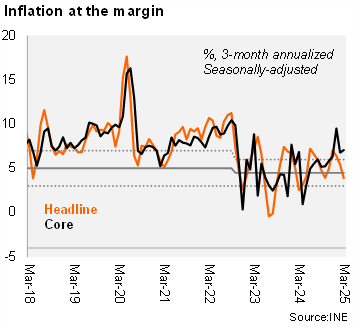

At the margin, headline inflation decelerated, while the core reading accelerated in March. Using our own seasonally adjusted figures, the three-month annualized headline inflation fell to 3.9% in March (from 5.4% in February), while core inflation was 7.1% (from 6.8% in the previous month).

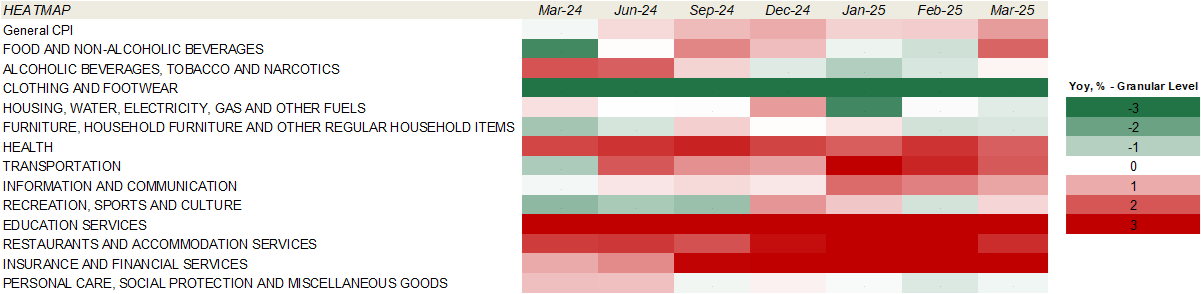

Our CPI heatmap shows that 31% of selected items are below the center of the central bank’s target (4.5%), down from 54% in February.

Our take: Our YE25 inflation forecast stands at 5.5%, but with a downside risk. Wage negotiations, set to take place in the second half of the year, will be important for inflation and inflation expectations. April CPI will see the light of day on May 5, while the next policy meeting (the first under the new BCU´s board) will be held next week, on April 8 in which we expect a 25-bps hike to 9.25%.