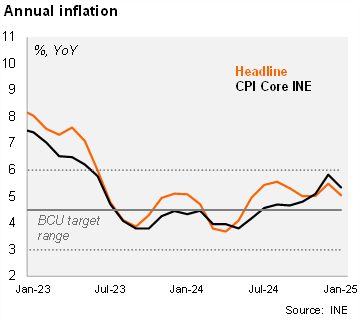

Headline inflation rose by 1.1% MoM in January (from 1.5% a year ago and a 5-year median figure of 1.7%). The print was below our forecast (1.4%) and market expectations according to the BCU’s survey (1.3%). The main monthly impacts came from food and non-alcoholic beverages which increased by 0.77% mom (incidence 0.2 p.p.) driven by higher meat prices. Moreover, housing, electricity, and water rose by 1.25% MoM (incidence of 0.16 p.p.), mainly explained by the positive effect of the application of the second part of the "UTE rewards" program on electricity (electricity supply fell 1.38% MoM). It is important to note that this discount will end in February. In addition, hotels and restaurants rose by 2.43%, transport rose by 0.24% mom mainly due to the increase in fuel prices. Core inflation (excluding fruits & vegetables and fuel prices) increased by 0.98% MoM, from 1.45% MoM in January 2024. On an annual basis, headline inflation fell to 5.05% in January (from 5.49% in December), while core inflation fell to 5.35% from 5.83% in the previous month. We note that both readings remain within the Central Bank's inflation target of 4.5% +/- 1.5%.

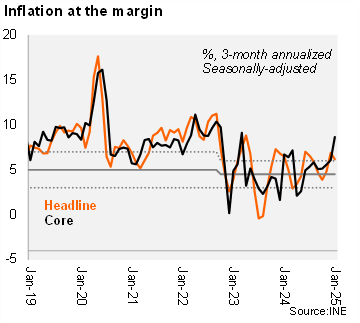

At the margin, headline inflation decelerated in January while the core accelerated. Using our own seasonally adjusted figures, the three-month annualized headline inflation fell to 6.2% in January (from 6.9% in December), while core inflation was 8.7% (from 6.1 in the previous month).

Our CPI heatmap shows that 38% of selected items are below the center of the central bank’s target (4.5%).

Our take: We foresee inflation at 6.0% by YE25, at the upper bound of the central bank’s inflation target range. Although CPI came in lower than expected in January, we expect the central bank's board to raise the policy rate by 25 bps to 9.0% on February 13, given the recent deterioration in inflation expectations. The CPI for February will see the light on March 5.